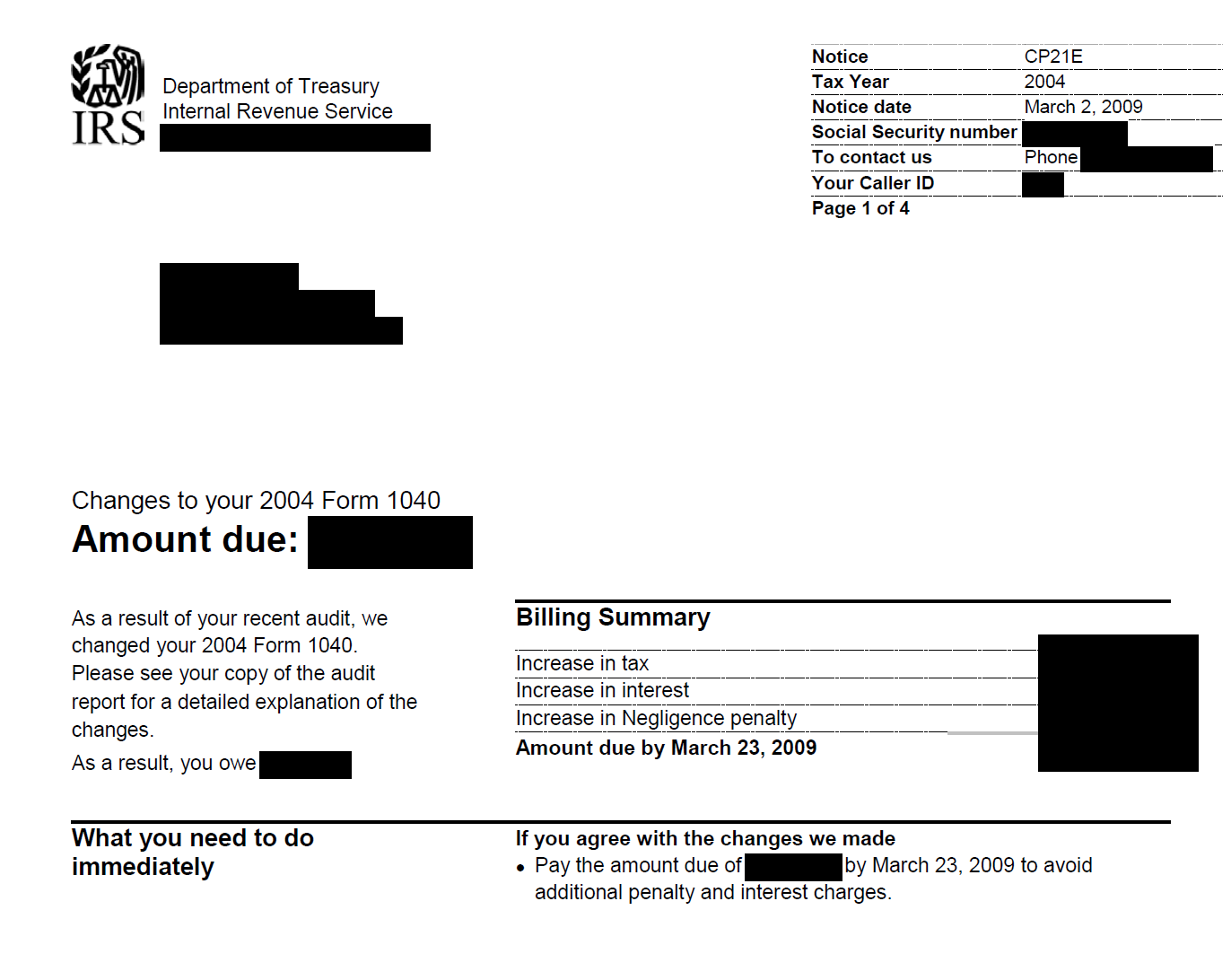

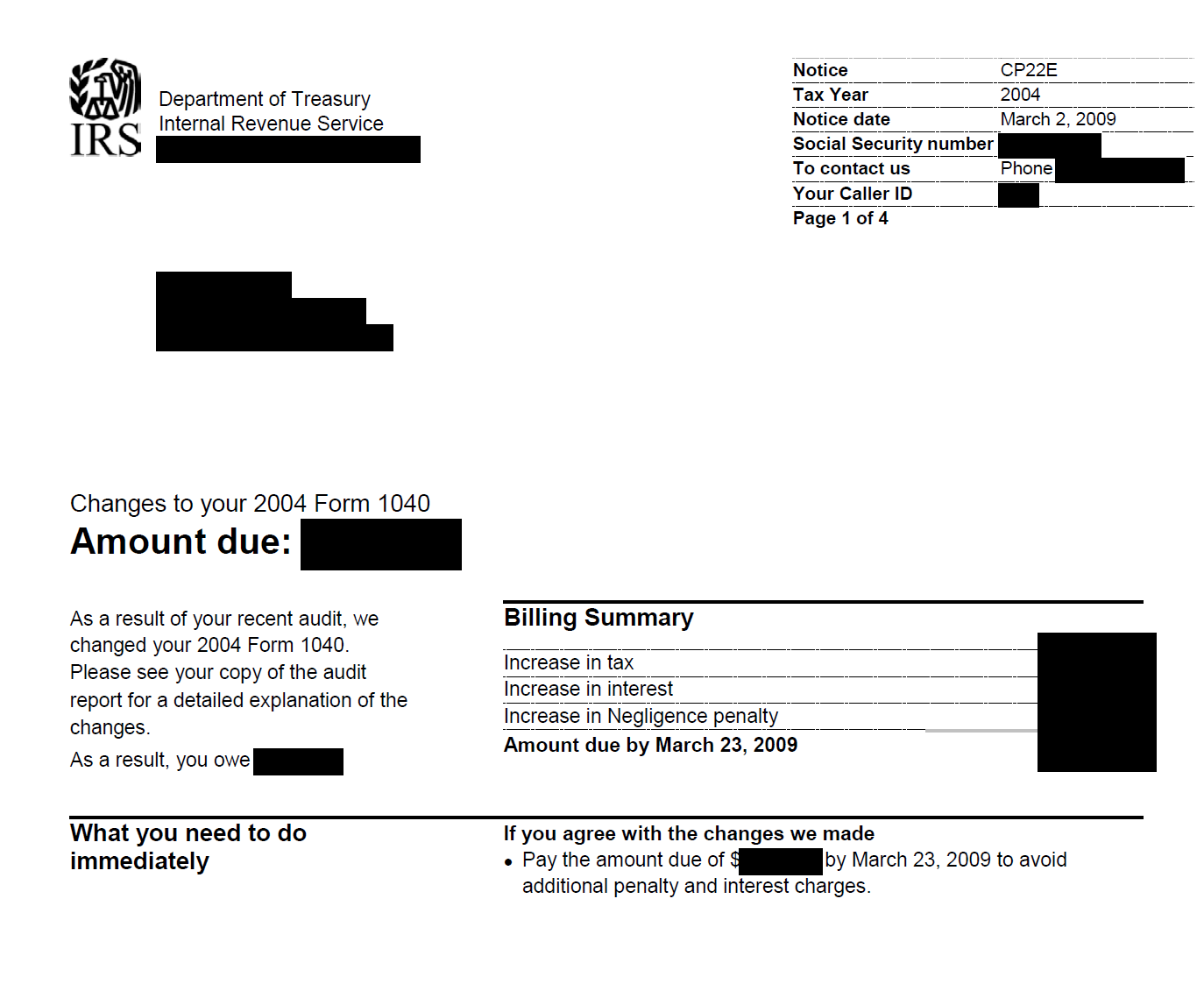

CP22E: Assessment from a CP2000

Balance due from the AUR adjustment. [IRM 3.14.1.6.18.1.1 (1-1-2015)]

Updated: June 23, 2025

Tax Problems and Solutions Handbook

Tax Problems and Solutions Handbook

Balance due from the AUR adjustment. [IRM 3.14.1.6.18.1.1 (1-1-2015)]

Updated: June 23, 2025

Balance due from the AUR adjustment. [IRM 3.14.1.6.18.1.1 (1-1-2015)]

Updated: June 23, 2025

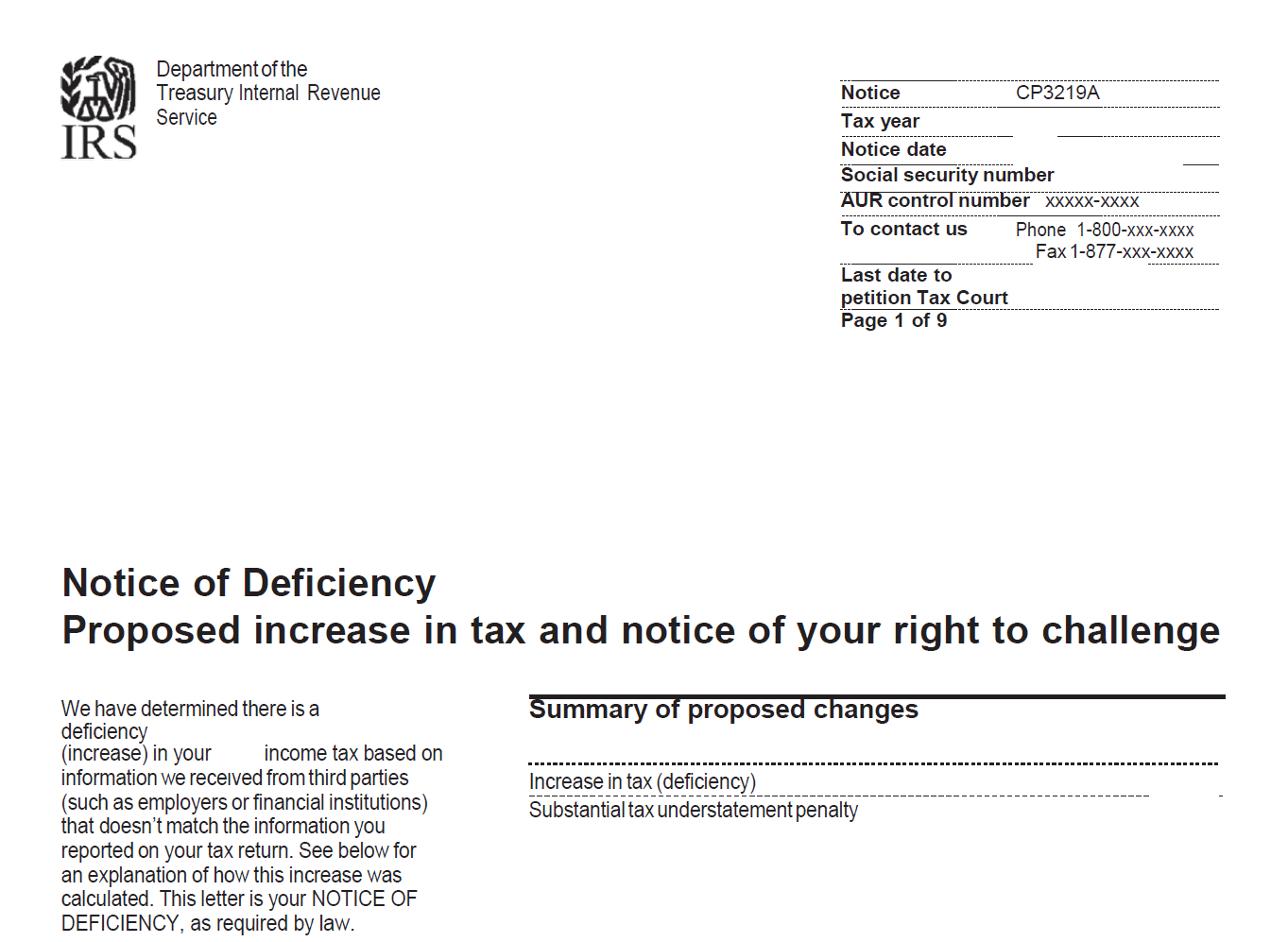

Statutory Notice of Deficiency, required by law, informs the taxpayer of the tax assessed, plus penalties and interest, that he or she owes. This letter also advises the taxpayer of appeal rights to the U.S. Tax Court.

Updated: June 23, 2025

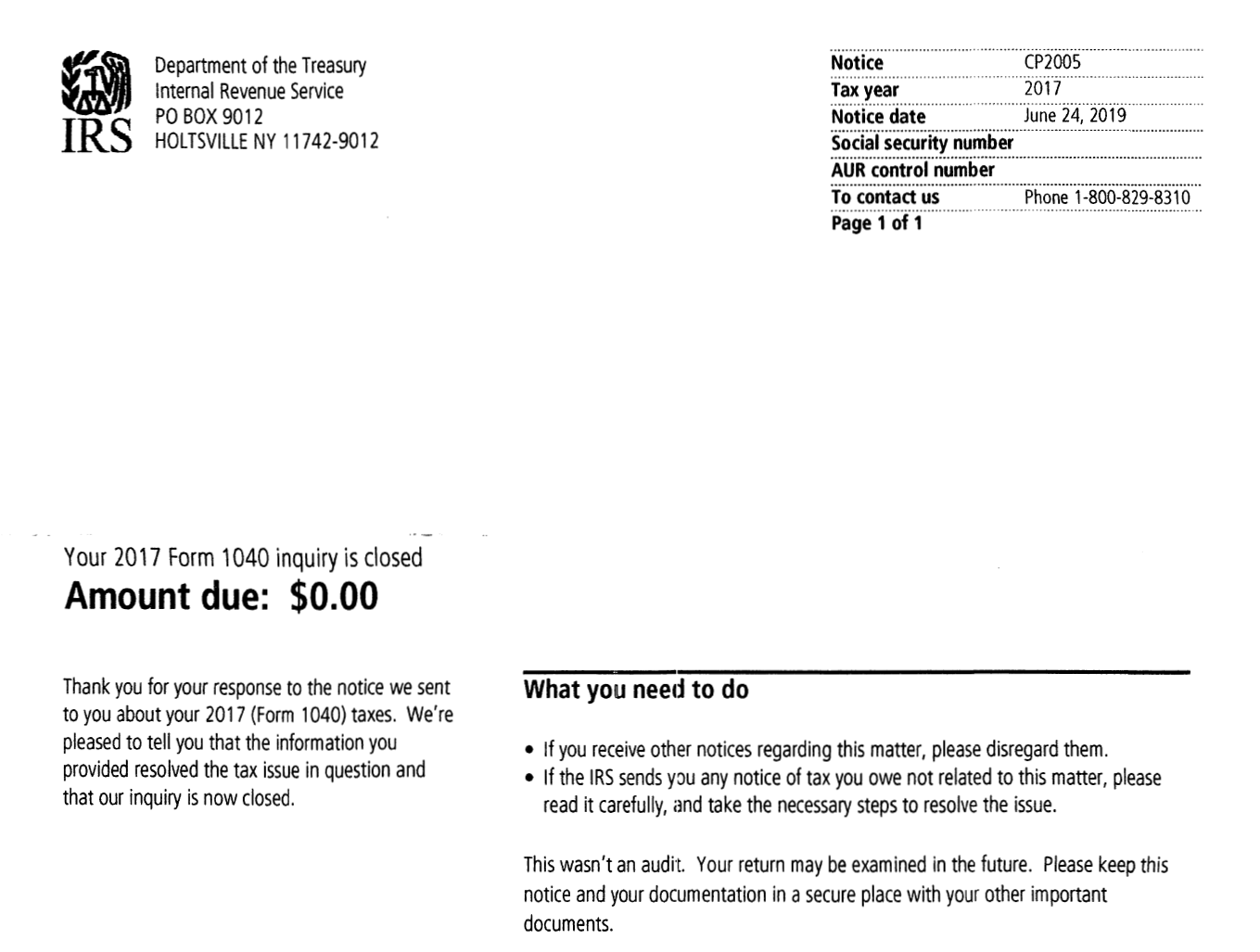

AUR Inquiry is closed with no change to the tax liability and/or refundable credits.

Updated: June 23, 2025

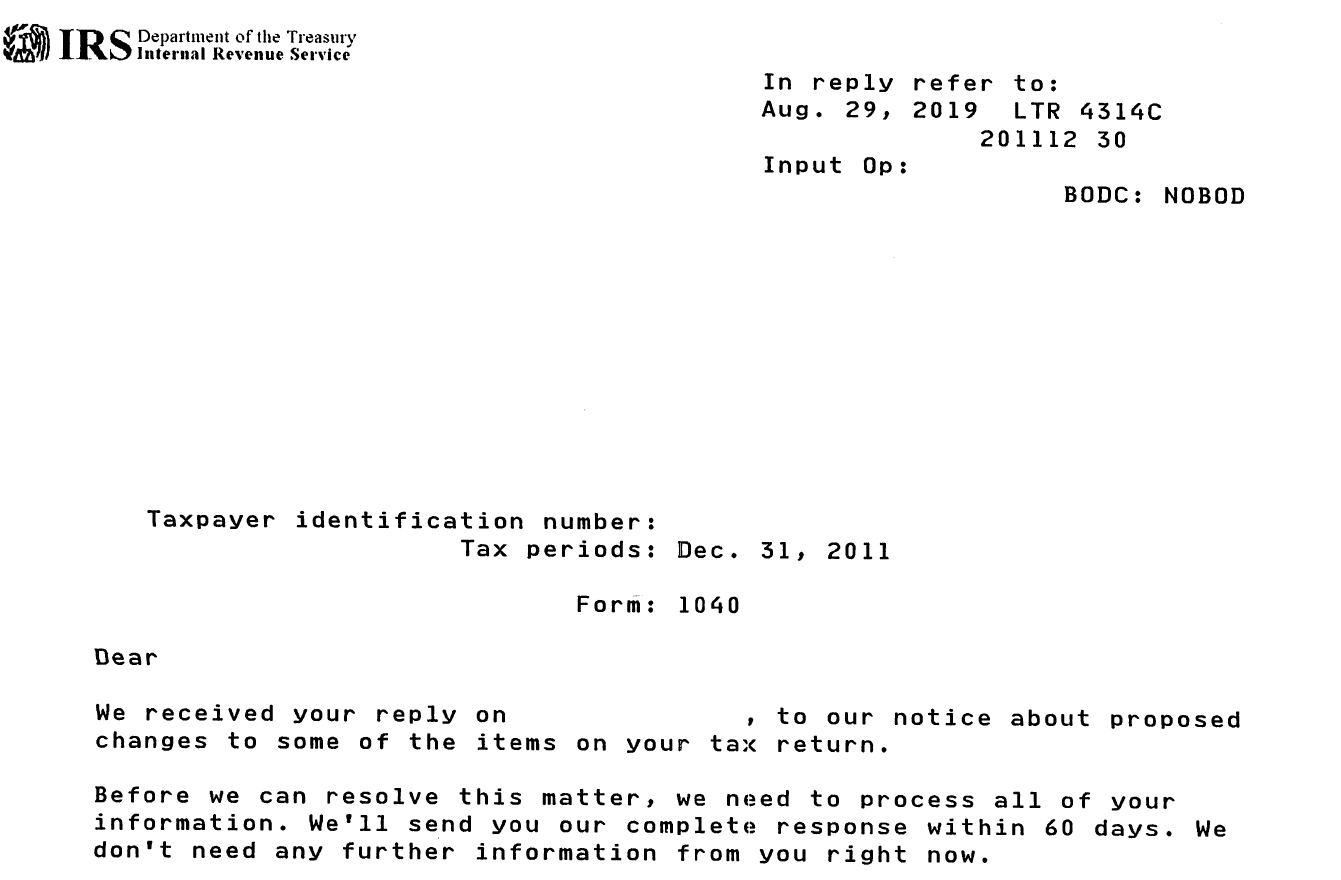

When a quality response cannot be issued timely, an automatic, interim response is sent the 30th calendar day from the IRS-received date. [IRM 4.19.2.3.1 at (2) (9-12-2024)]

Updated: June 23, 2025

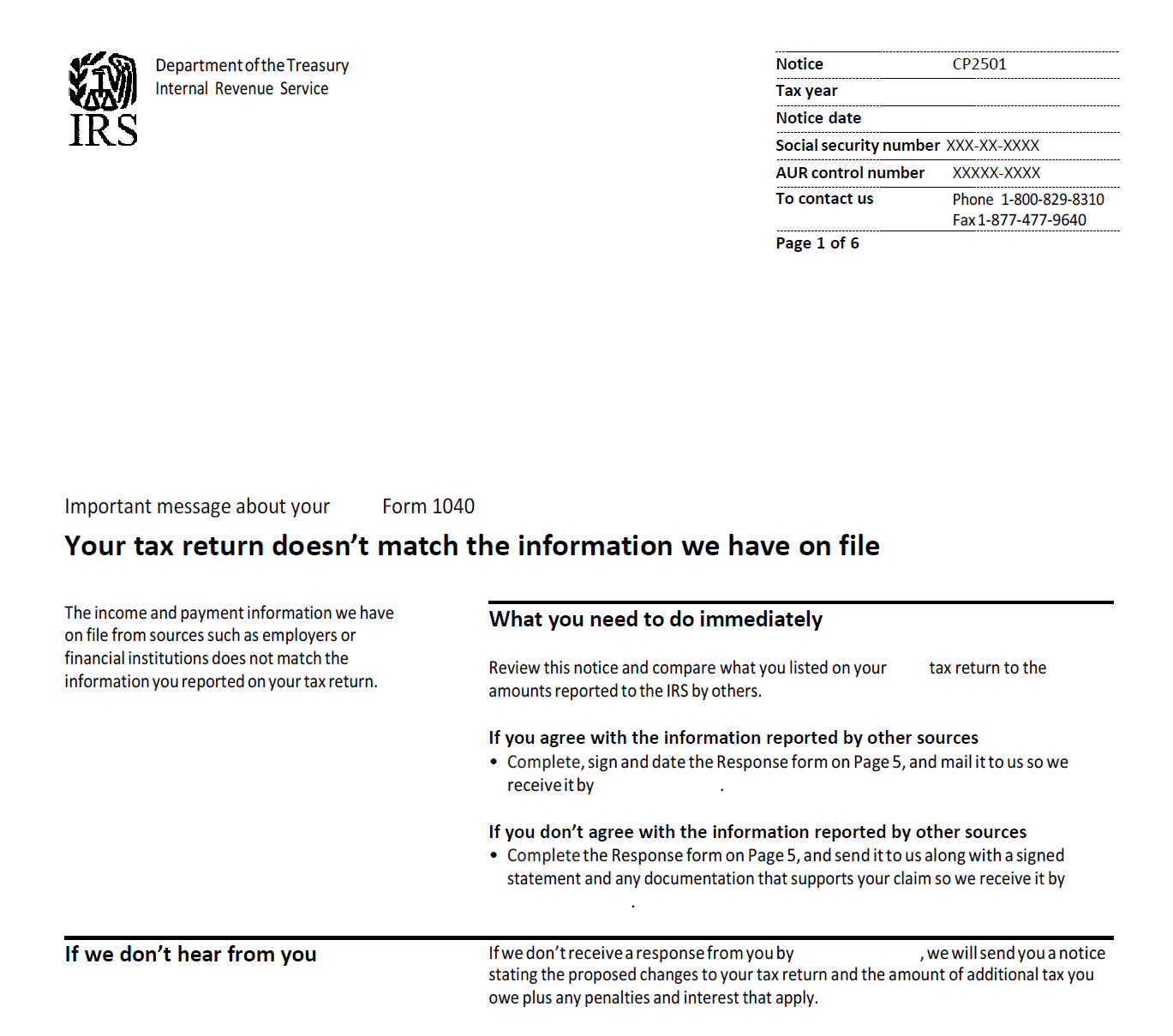

Pre-CP2000 Contact Letter. In certain situations, an initial notice sent to the taxpayer requesting an explanation to resolve a discrepancy between items reported by the taxpayer on the tax return and the information provided by third parties regarding those items. If the taxpayer fails to respond or if the response is insufficient, the Service sends a CP2000 notice proposing an adjustment. [IRM Exhibit 1.4.19-1]

Updated: June 23, 2025

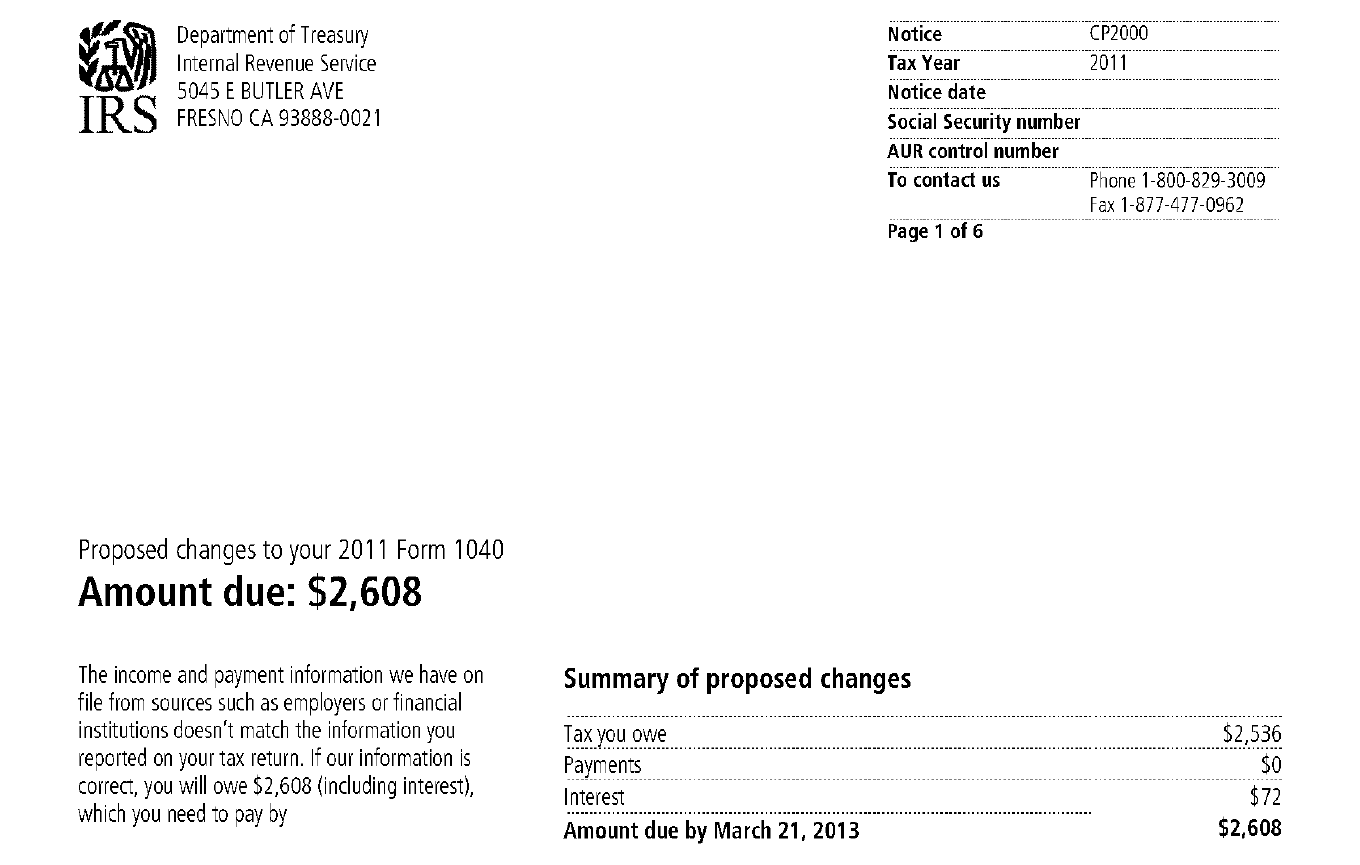

Notifies taxpayer of a proposed change to tax liability because of income that is not identifiable or apparently not fully reported on the return and/or credits and deductions that appear overstated.

Updated: June 23, 2025