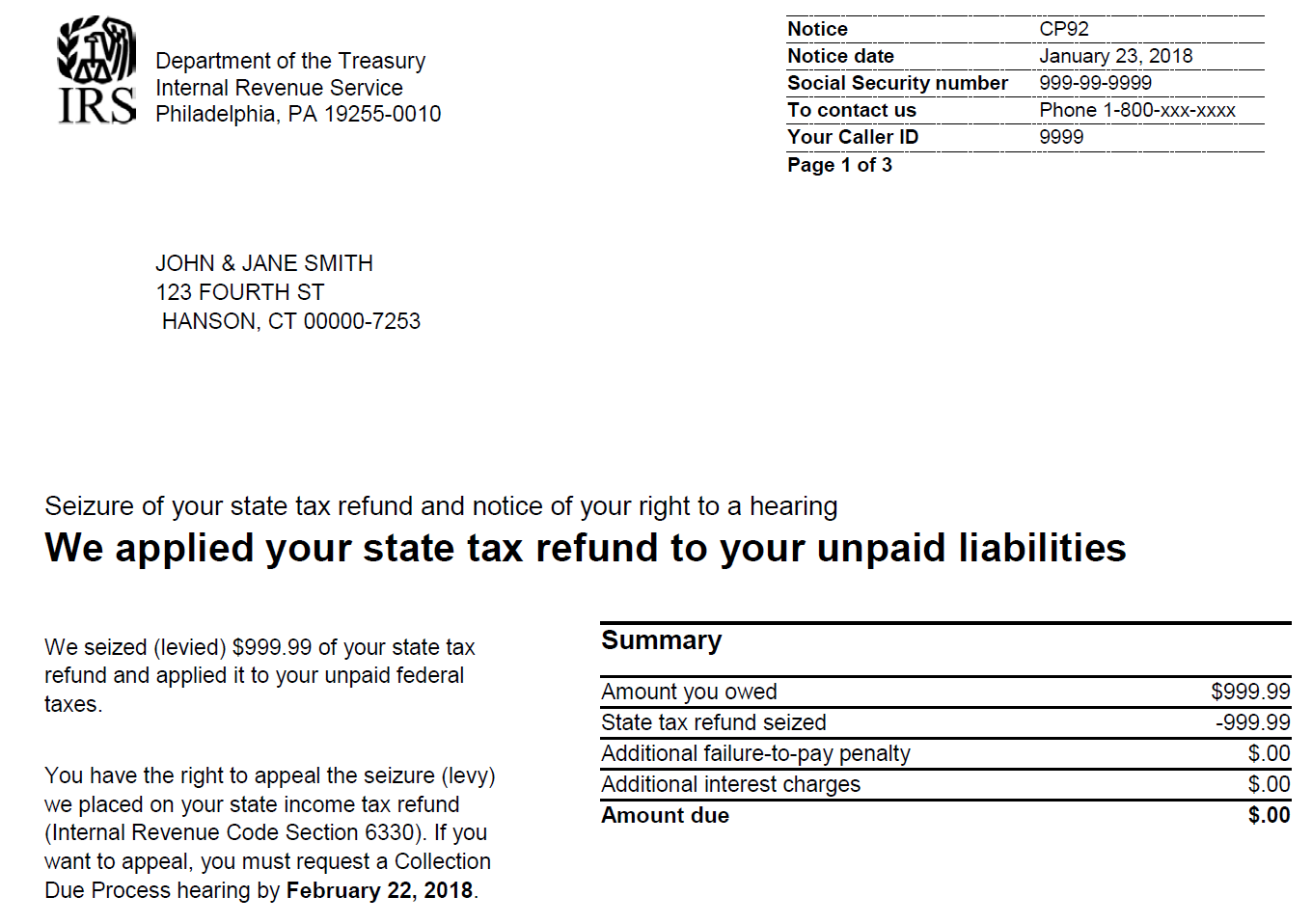

CP92: Notice of Levy on Your State Tax Refund- Notice of Your Right to a Hearing

Notification of state income tax levy

Updated: July 14, 2025

Tax Problems and Solutions Handbook

Tax Problems and Solutions Handbook

Notification of state income tax levy

Updated: July 14, 2025

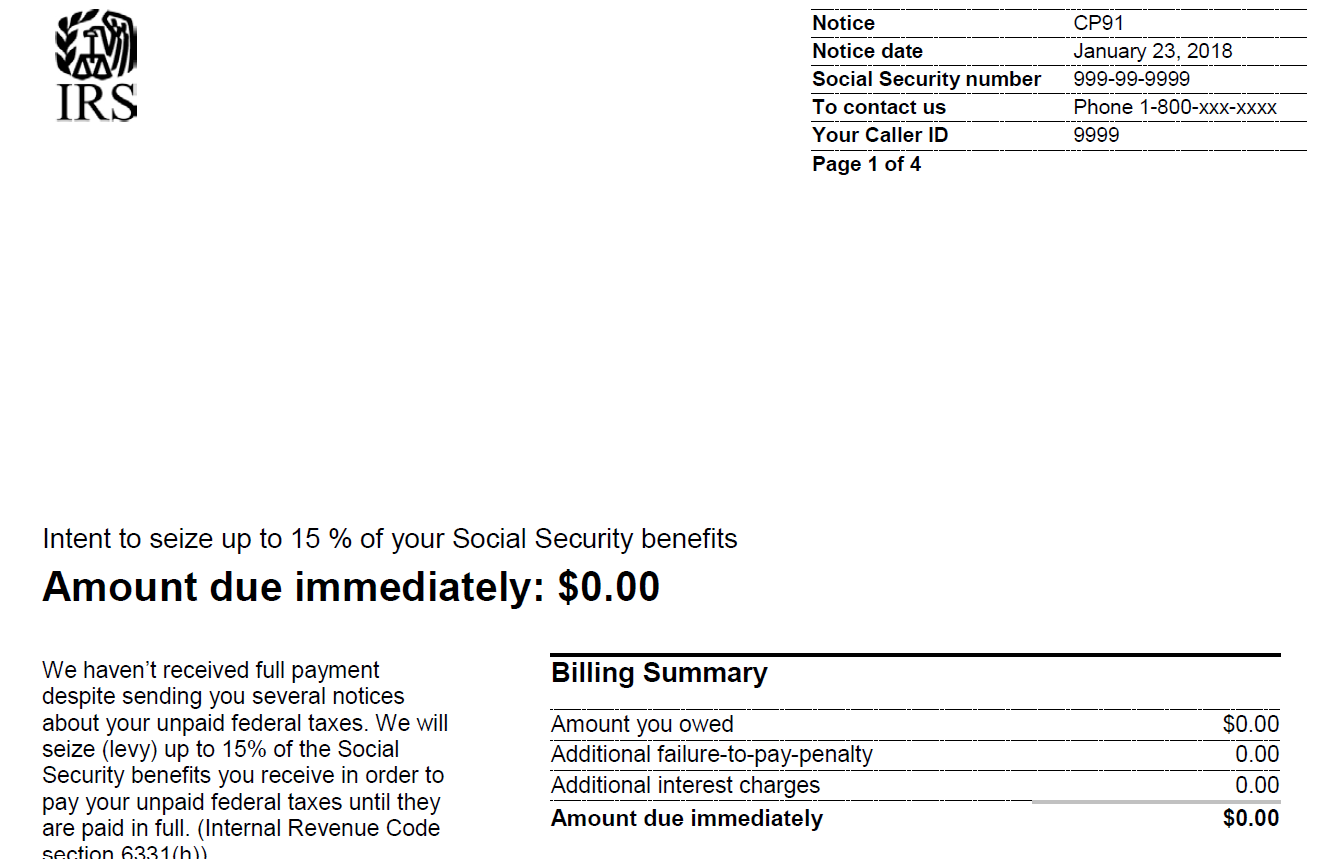

Notie of intent to seize 15% of social security benefits

Updated: July 14, 2025

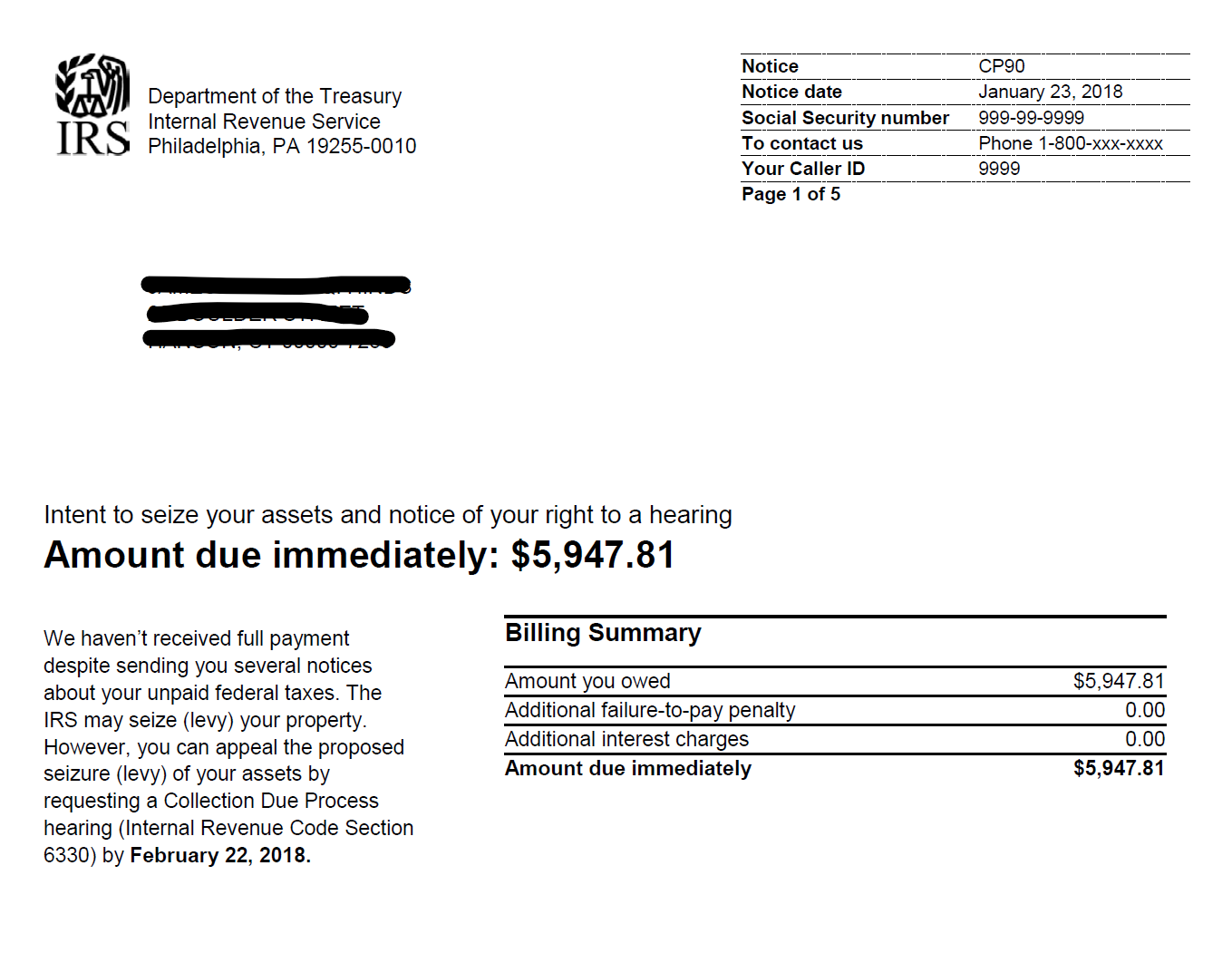

Notice of Intent to Levy on a federal payment

Updated: July 10, 2025

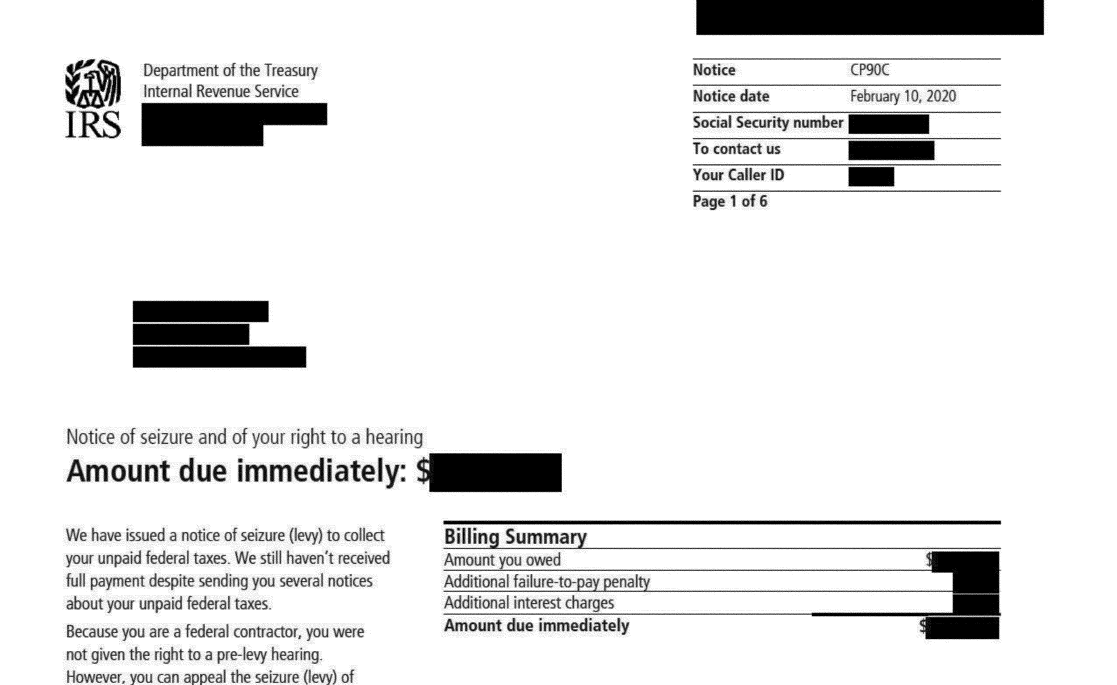

Notice of intent to seize assets on a federal payment

Updated: July 14, 2025

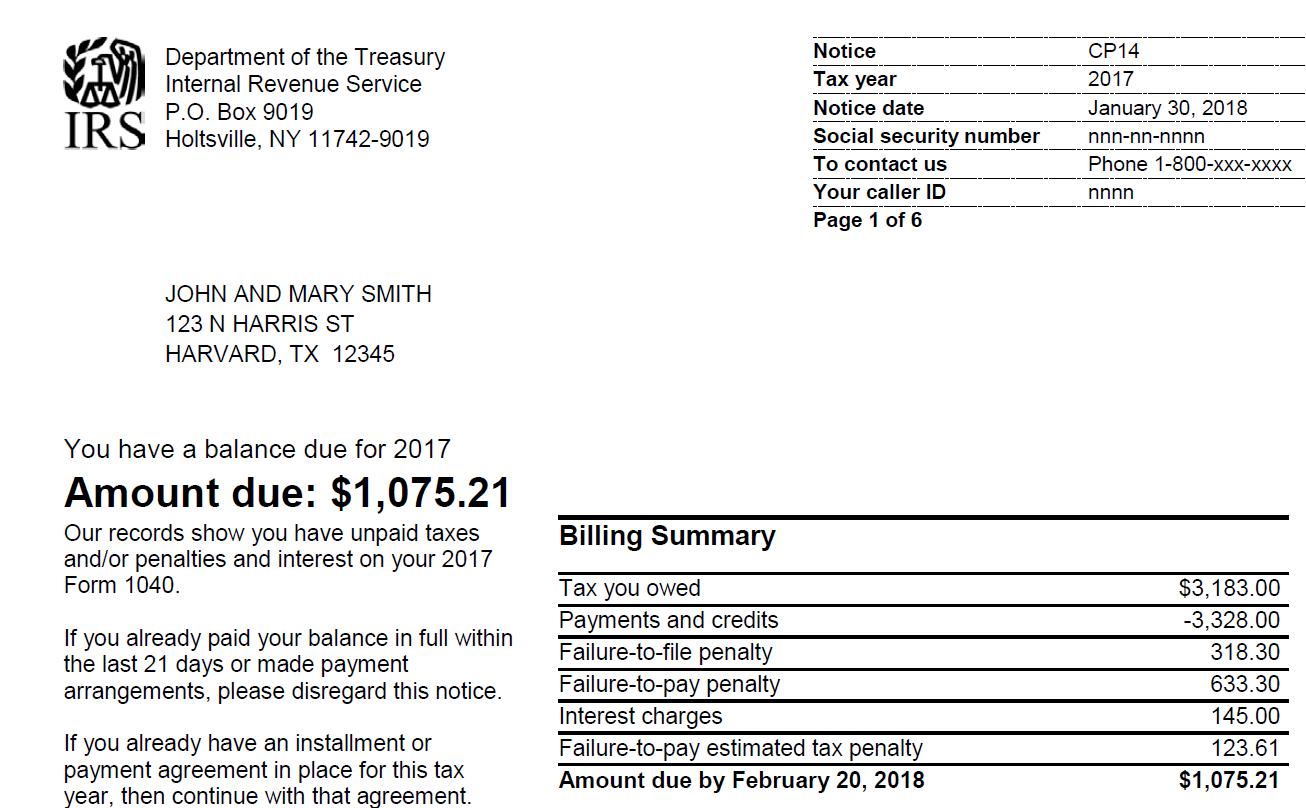

First balance due notice

Updated: July 10, 2025

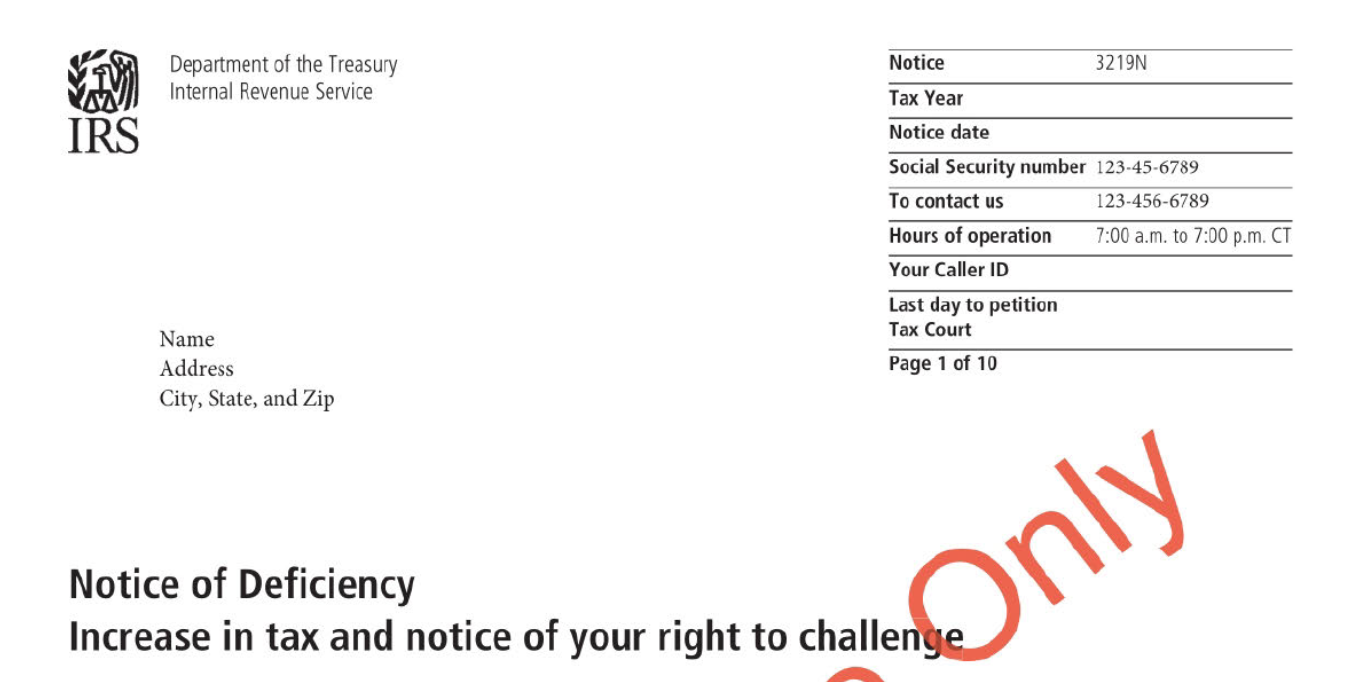

SFR 90-day letter. The taxpayer is given another 90 days to respond or to seek judicial review before the proposed tax is assessed. The proposed tax computed by the IRS may be higher than what would actually be owed because the IRS cannot make an assessment that includes some exemptions, deductions, or credits the taxpayer must claim on a filed return. At this point, the taxpayer needs to file the return or the SFR proposed amount will be assessed in 90 days.

Updated: June 23, 2025

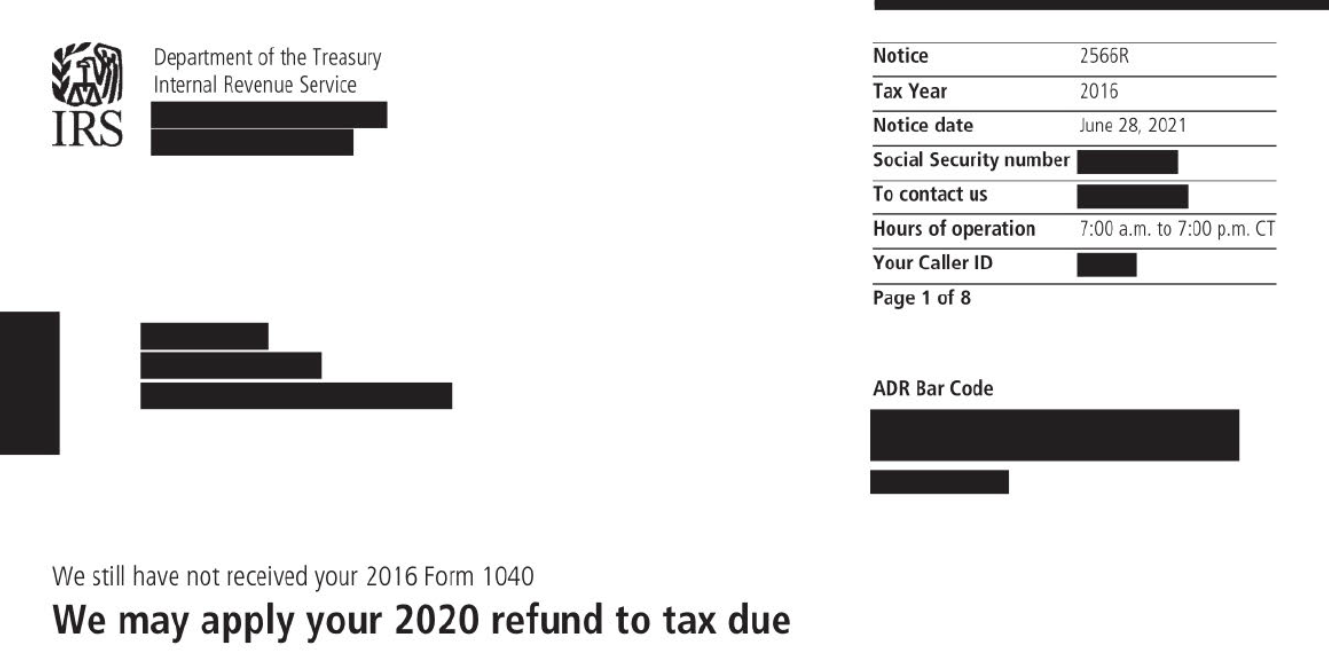

Same as Letter 2566. However, the taxpayer refunds are on hold until returns are filed.

Updated: June 23, 2025

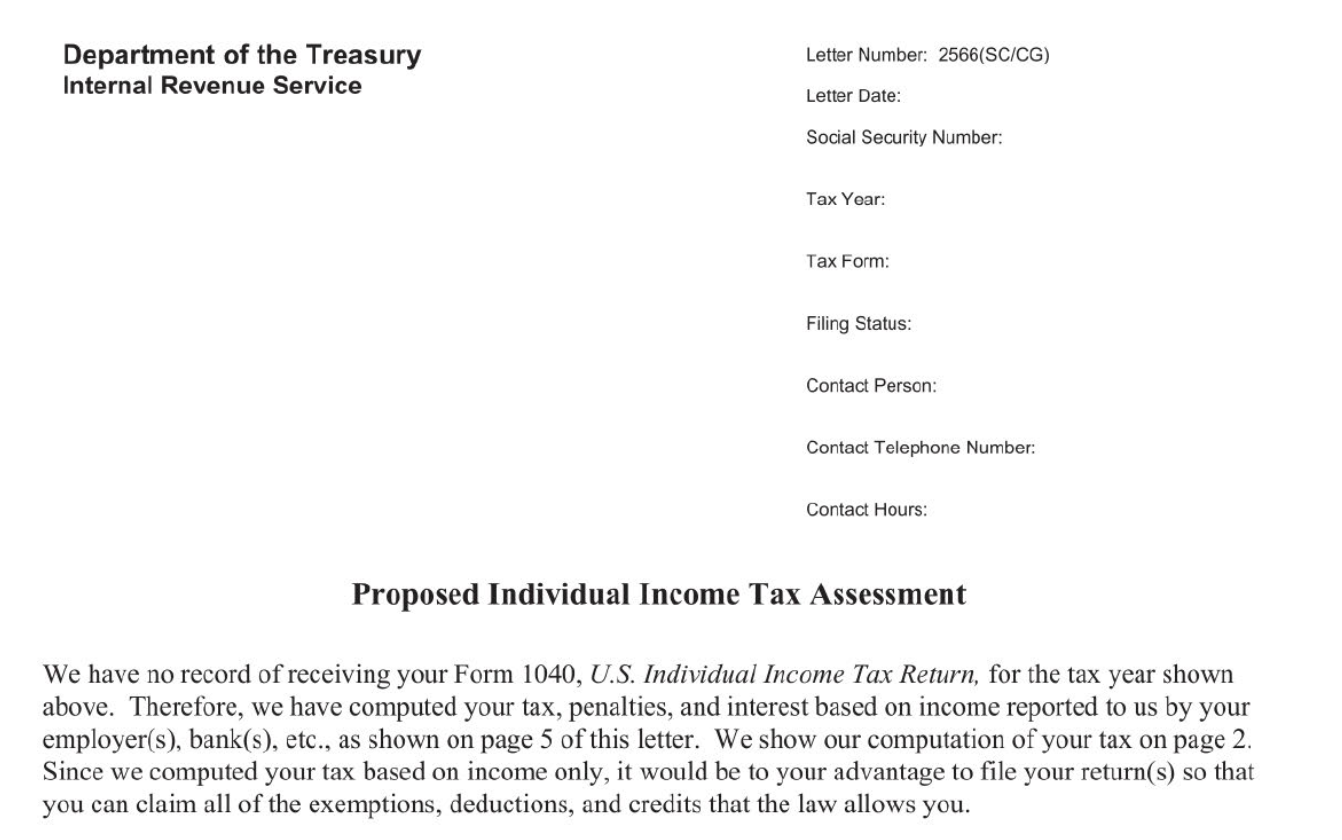

The letter informs the taxpayer that the IRS has not received a tax return for the tax year shown and includes a proposed tax assessment for the taxpayer. The letter advises taxpayers that within 30 days they must do one of the following: send their signed tax return, consent to the proposed tax assessment or explain why they believe they are not required to file.

Updated: June 23, 2025

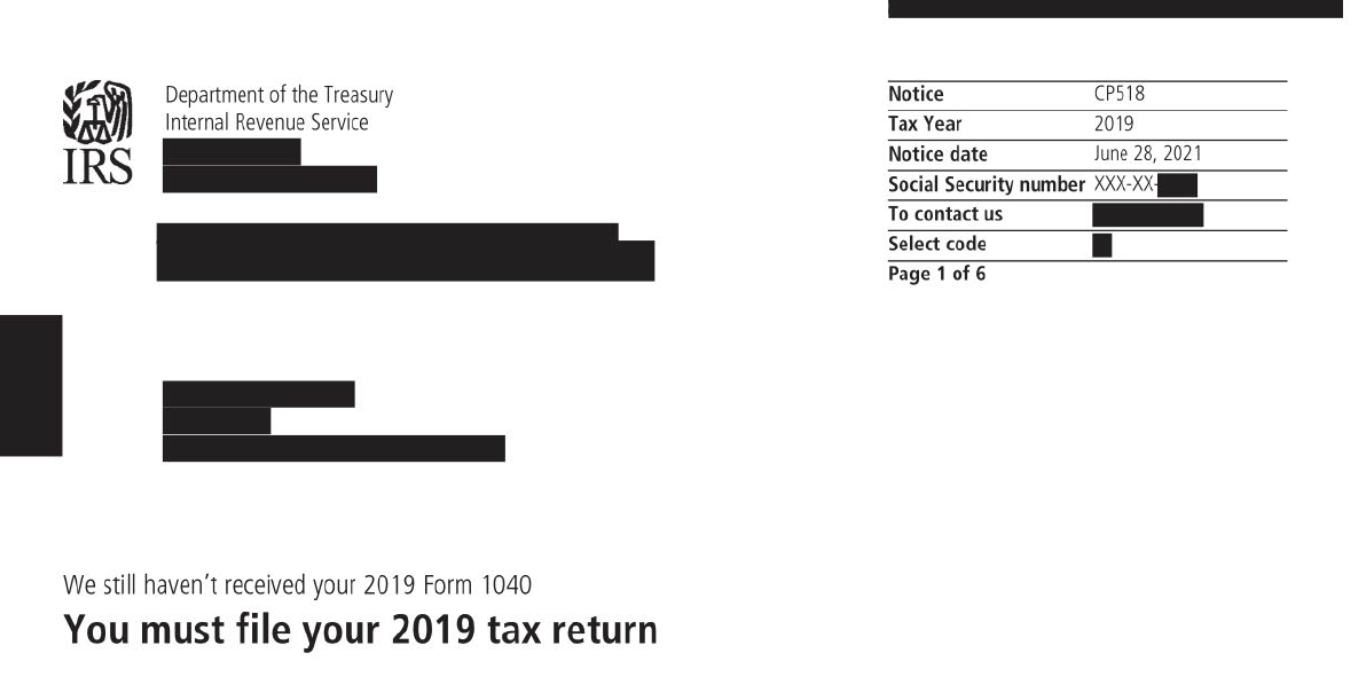

Final return delinquency notice — issued eight weeks after the CP59 (if no return is received). [IRM 5.19.2.3 (2-15-2022)]

Updated: June 23, 2025

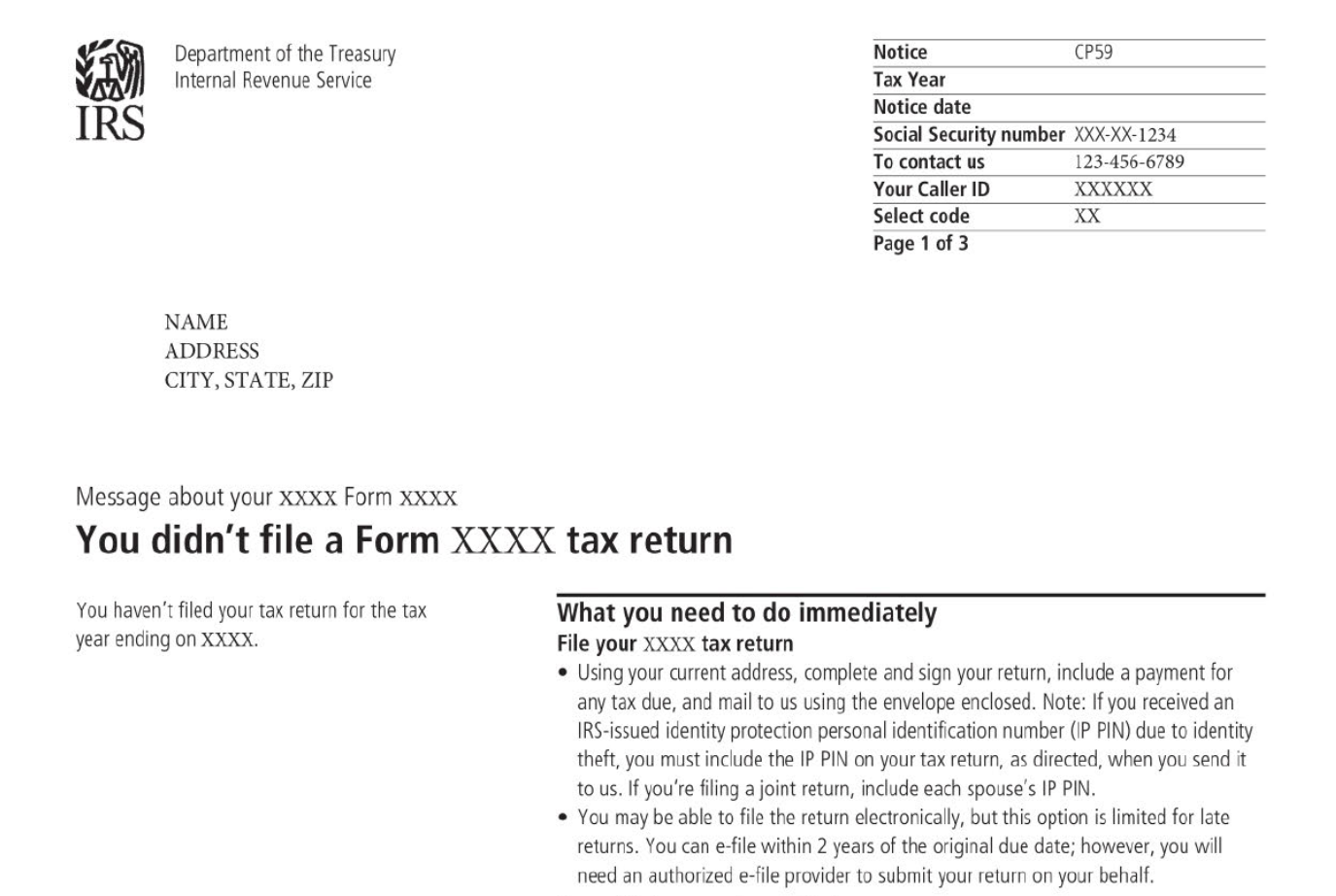

Initial return delinquency notice (issued after each tax year in November and the following February). [IRM 5.19.2.3 (2-15-2022) and IRM 5.19.2.6.2.1 (11-6-2015)]

Updated: June 23, 2025