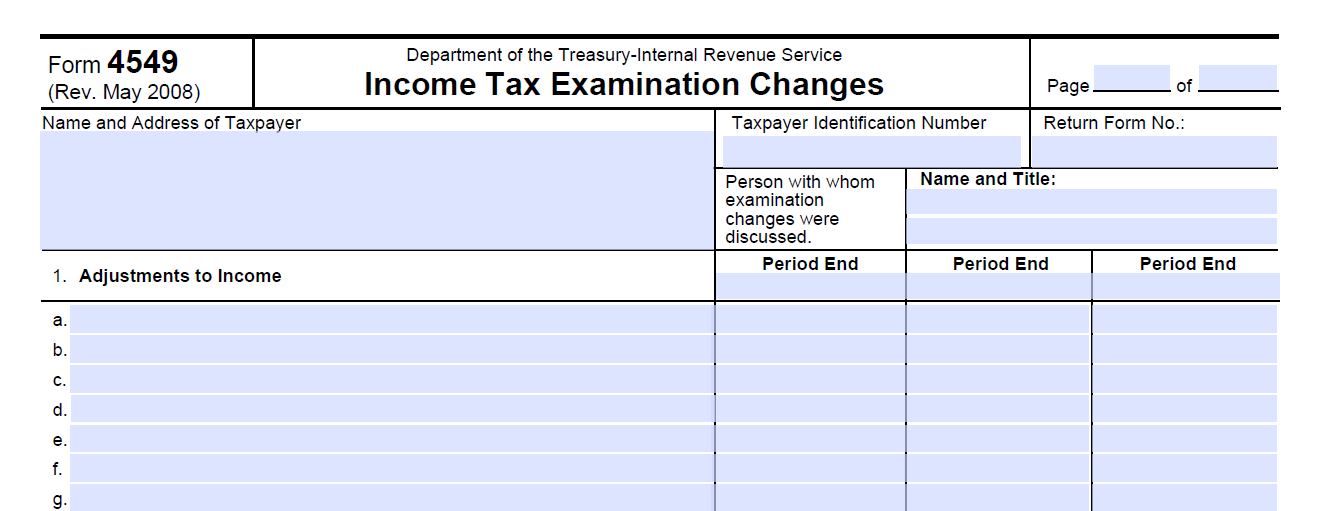

Form 4549: Income Tax Examination Changes

Provides audit adjustments, including penalties. Accuracy penalty will be on Line 17 of the Form. A supplemental Form 886-A will explain the IRS rationale for the penalty.

Updated: June 23, 2025

Tax Problems and Solutions Handbook

Tax Problems and Solutions Handbook

Provides audit adjustments, including penalties. Accuracy penalty will be on Line 17 of the Form. A supplemental Form 886-A will explain the IRS rationale for the penalty.

Updated: June 23, 2025

Notifies the taxpayer that penalty abatement was approved. Letter will state “because of good compliance history” if first-time abatement was granted.

Updated: June 23, 2025

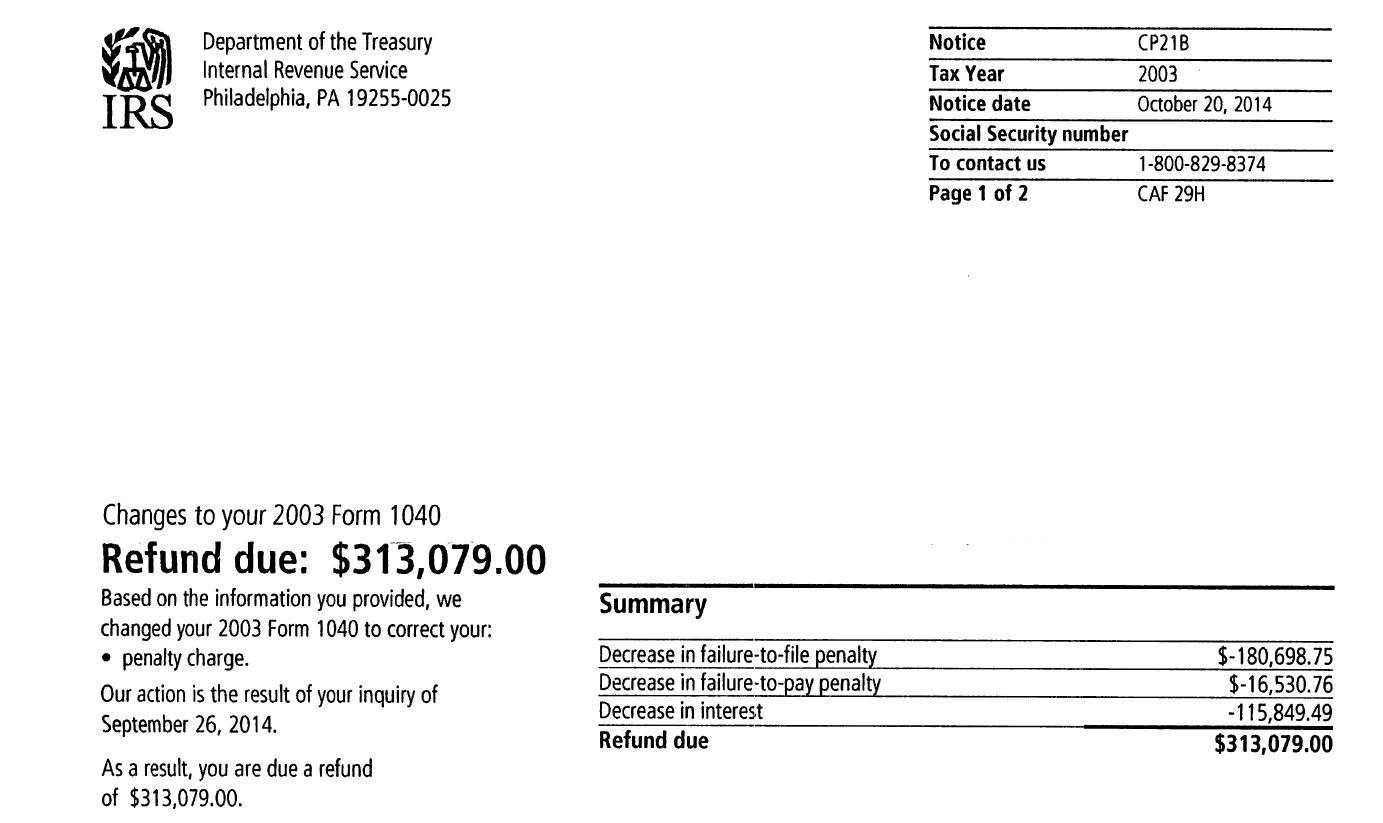

Notifies the taxpayer of the penalty amounts abated for the tax period.

Updated: June 23, 2025

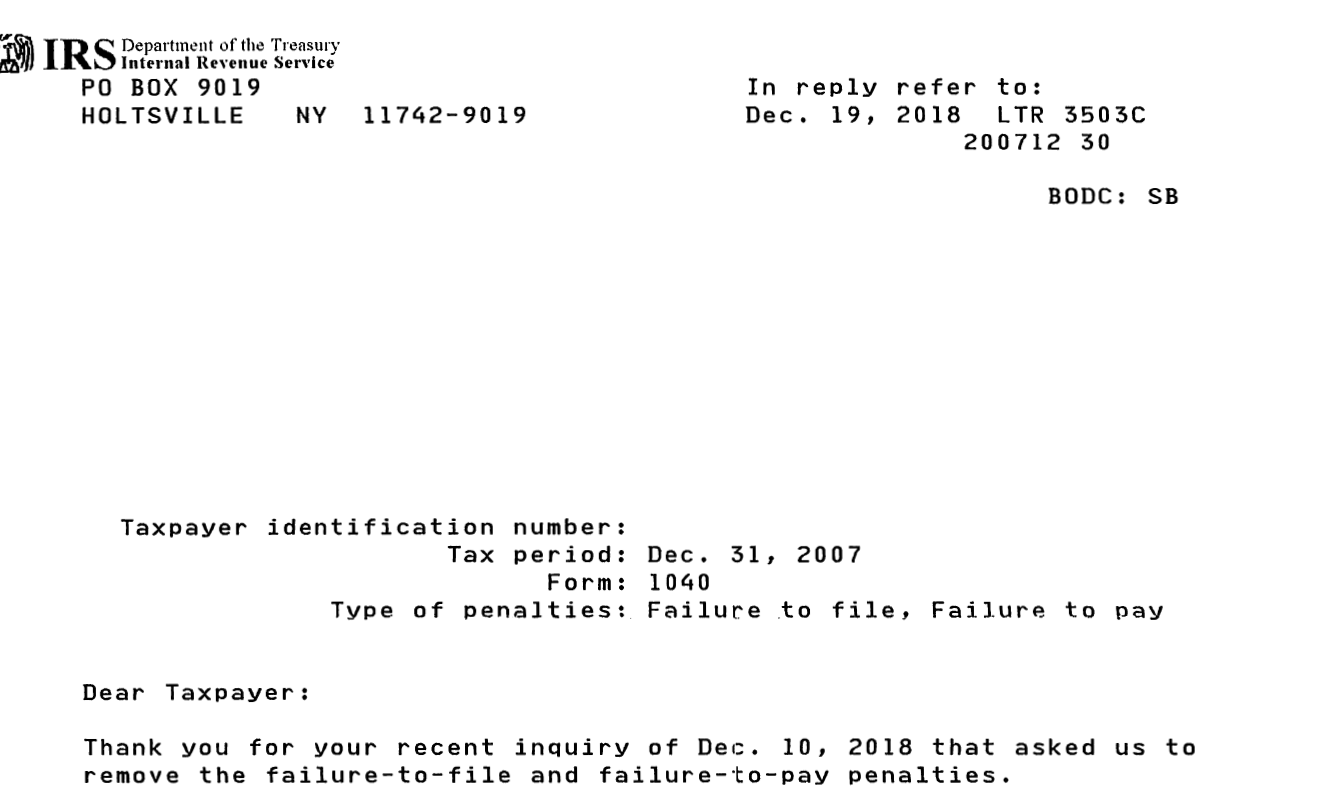

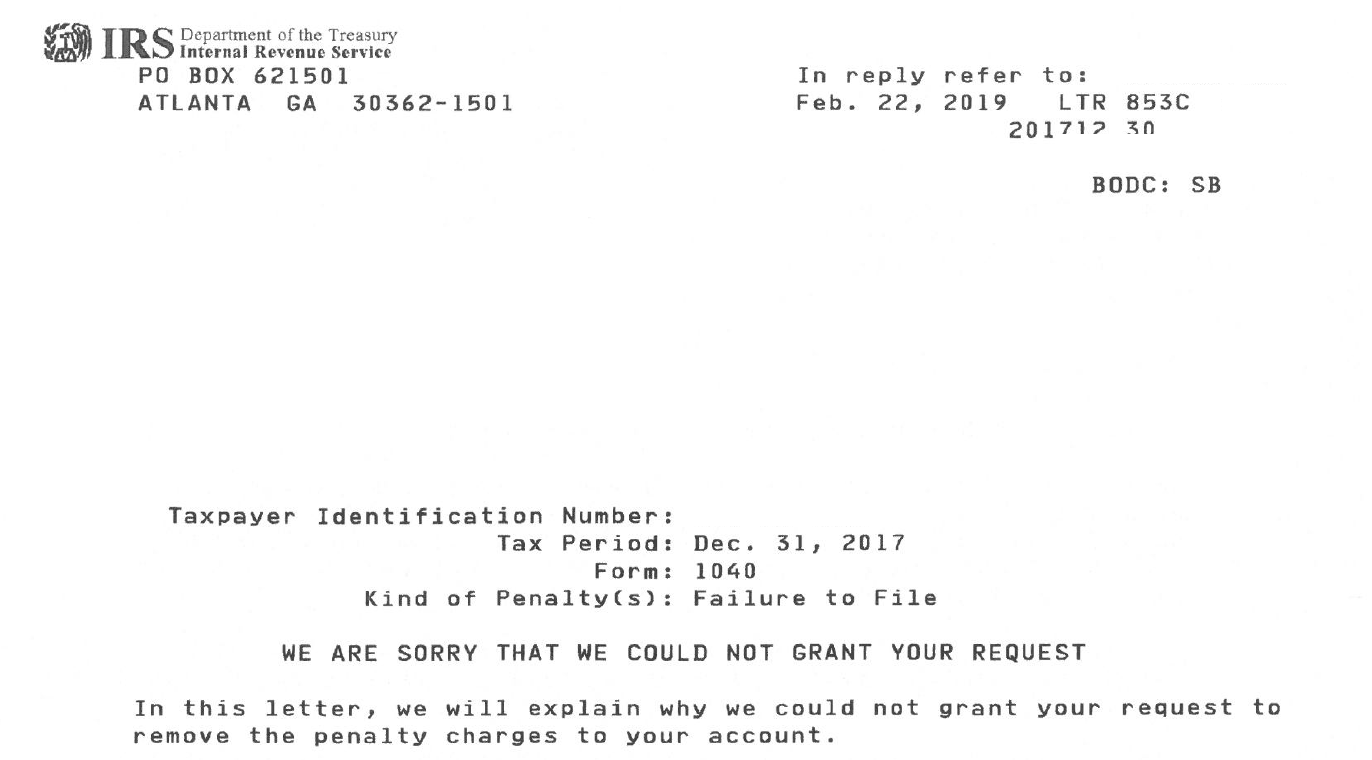

Denial letter version of 853C. Notifies the taxpayer that penalty abatement was denied. Provides reason(s) for denial.

Updated: June 23, 2025

Targeted soft notice to crypto-currency holder for 2013-2017 requesting the taxpayer to review and/or amend the return. No response is required, but the IRS may contact the taxpayer in the future about compliance.

Updated: June 23, 2025

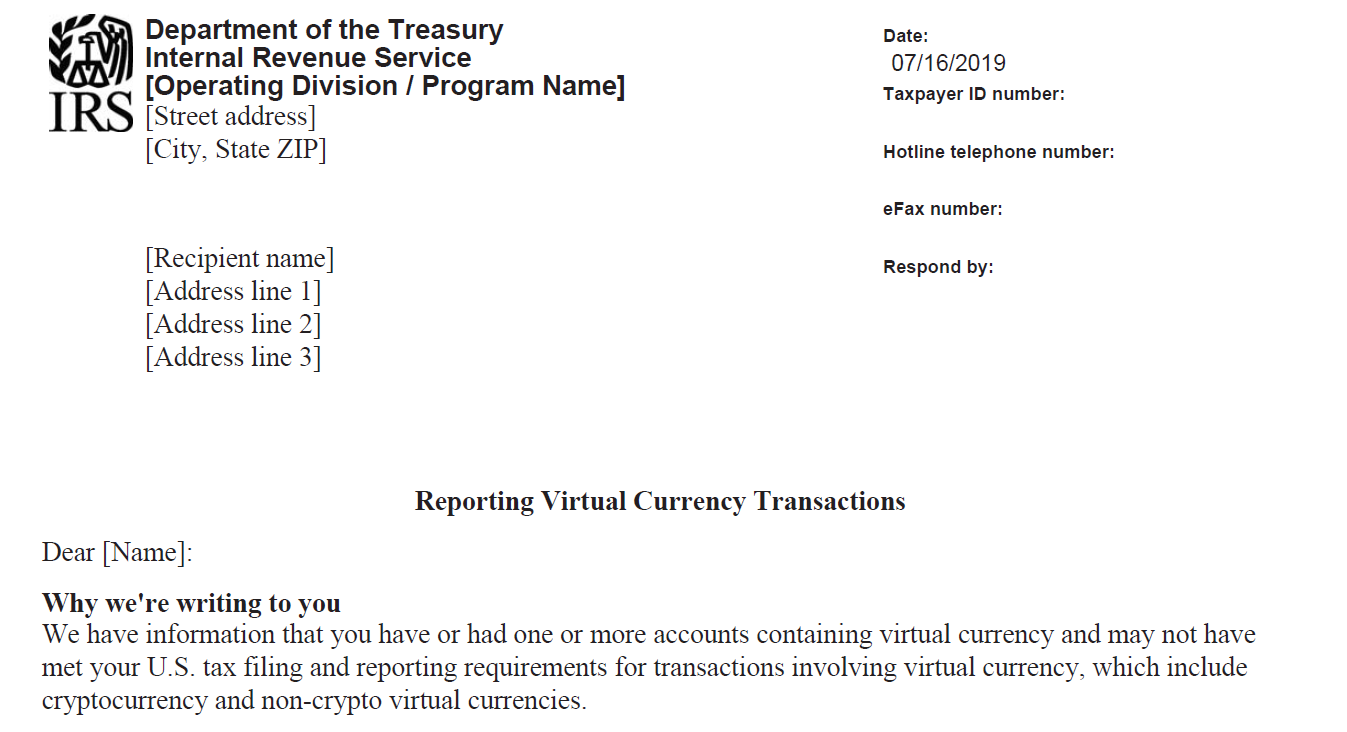

Targeted soft notice to crypto-currency holder for 2013-2017 requesting the taxpayer to review and/or amend the return. No response is required, and the IRS does not plan to follow up on the notice and/or response.

Updated: June 23, 2025

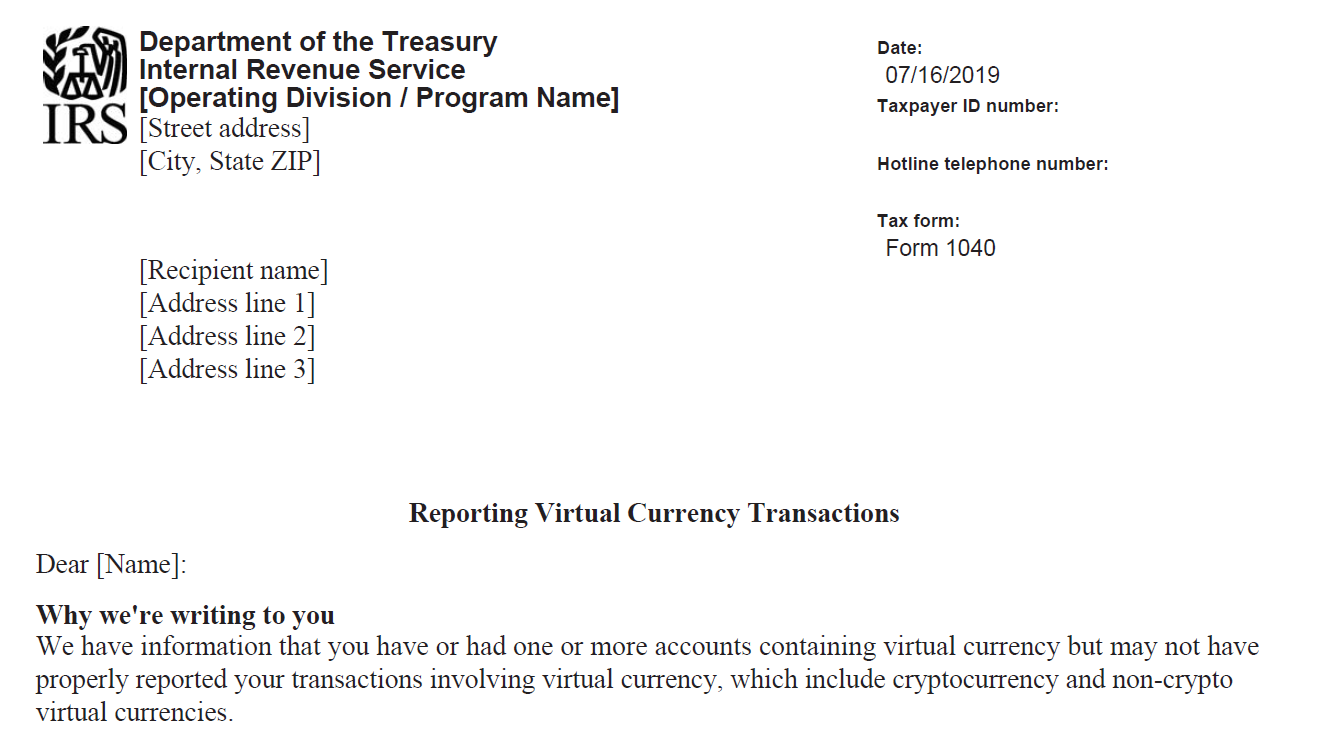

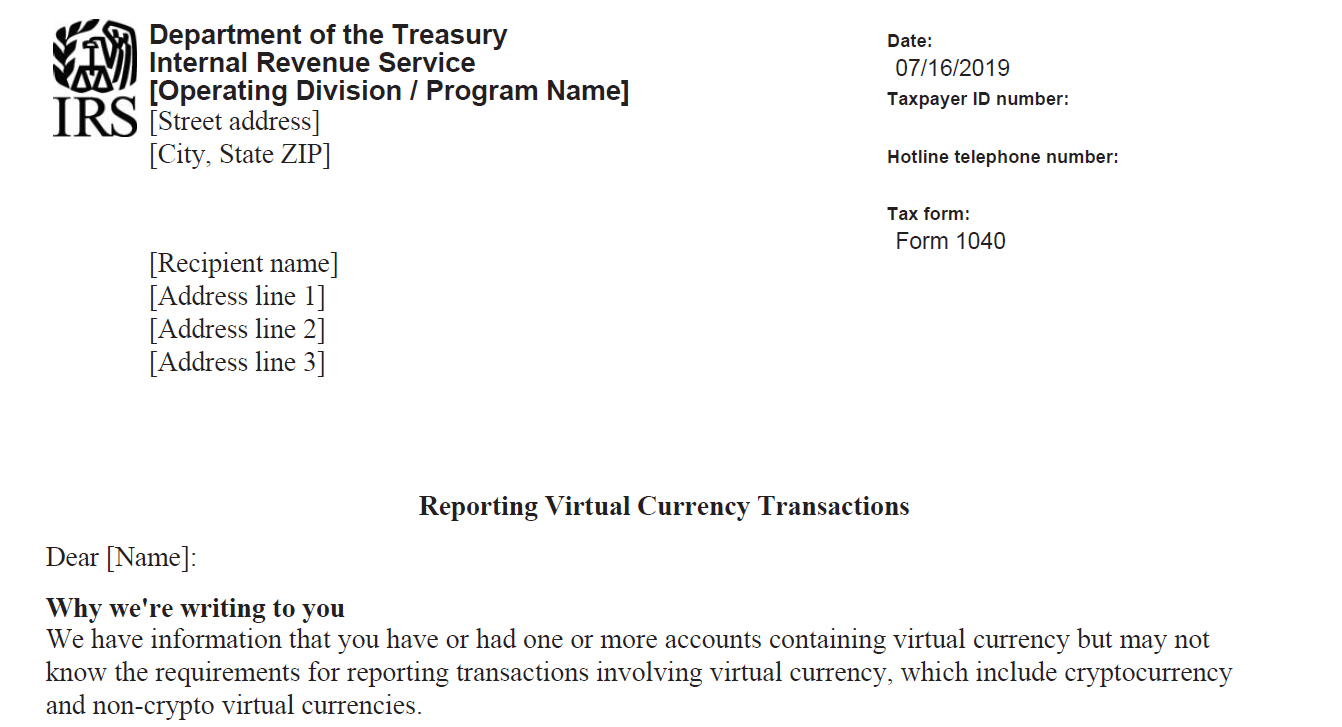

Targeted soft notice to crypto-currency holder for 2013-2017 requesting the taxpayer to file, review, and/or amend the return. A response is required from the taxpayer before the response date on the letter.

Updated: June 23, 2025

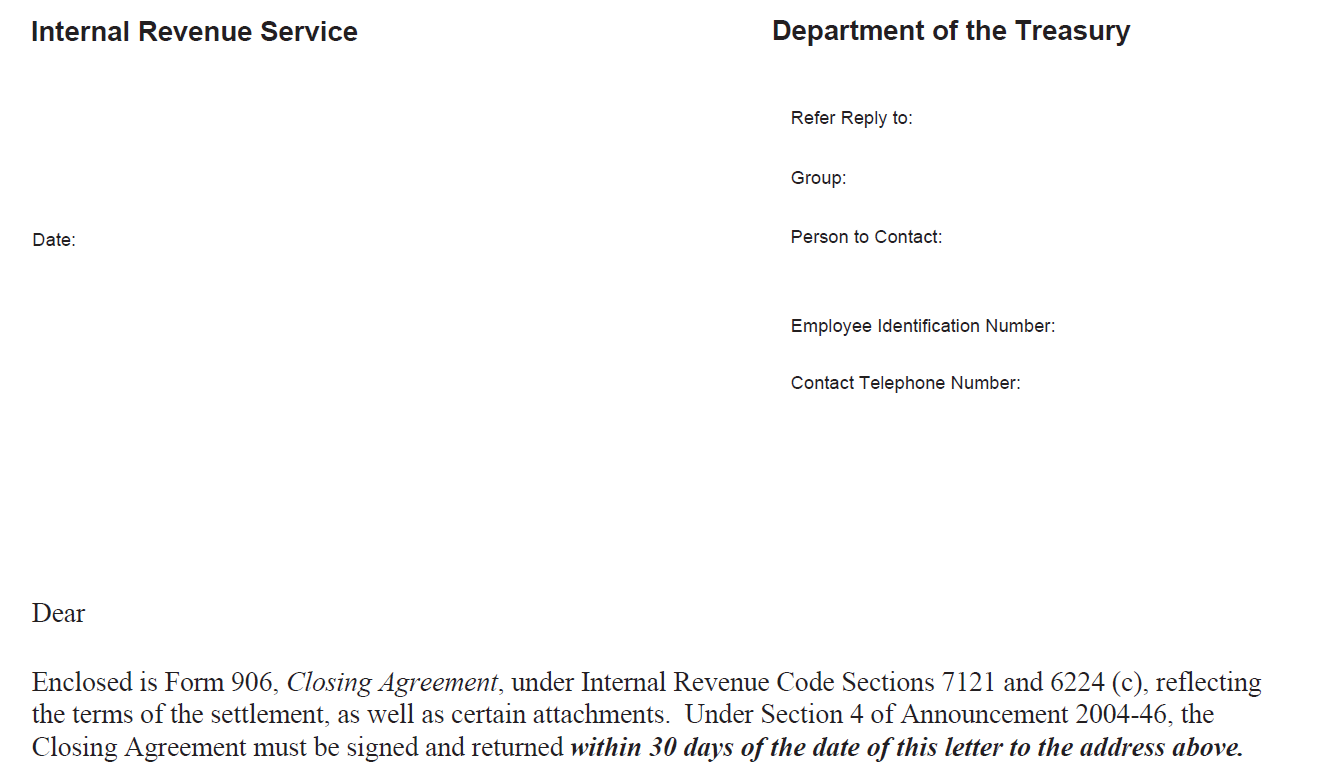

Appeals: Letter that accompanies a Closing Agreement settlement between the taxpayer and the IRS (Form 906). [IRM 8.20.7.13.2 (9-28-2018)]

Updated: June 23, 2025

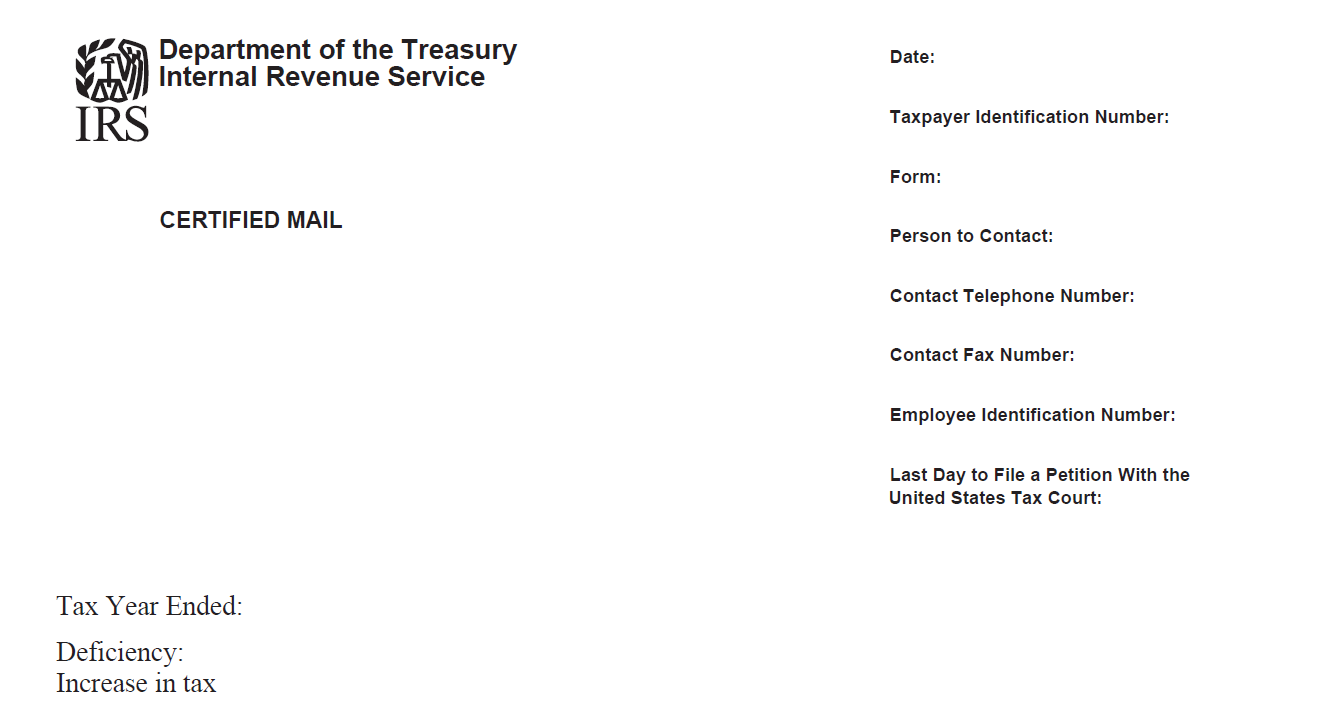

The Statutory Notice of Deficiency, required by law, informs the taxpayer of the tax assessed, plus penalties and interest, that he or she owes. This letter also advises the taxpayer of the appeal rights to the U.S. Tax Court. [IRM 4.8.9.9.3 (7-9-2013)]

Updated: June 23, 2025

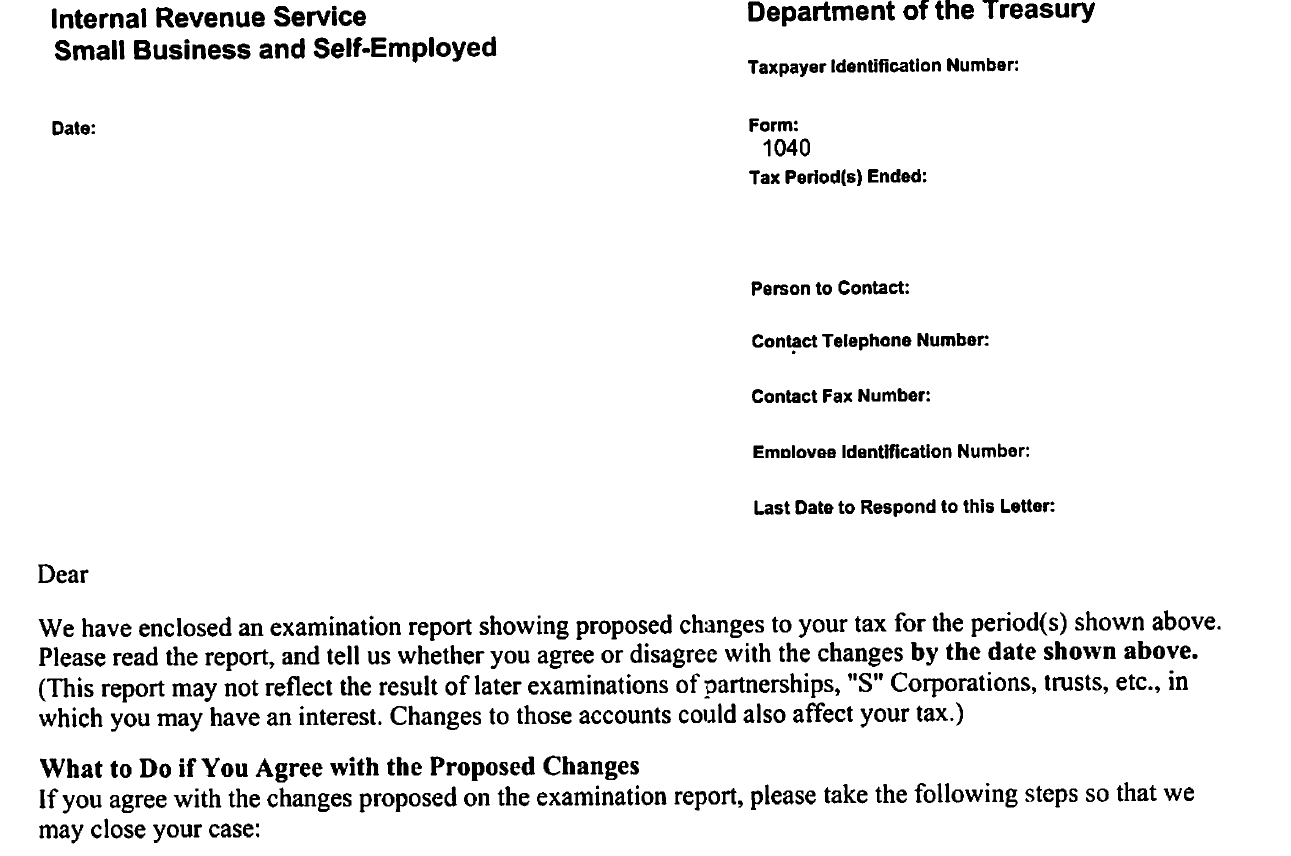

Field Exam: 30-day letter transmitting audit results where there was a change to the return. This notice allows the taxpayer the right to appeal. [IRM 4.10.8.12.1 (4-10-2023)]

Updated: June 23, 2025