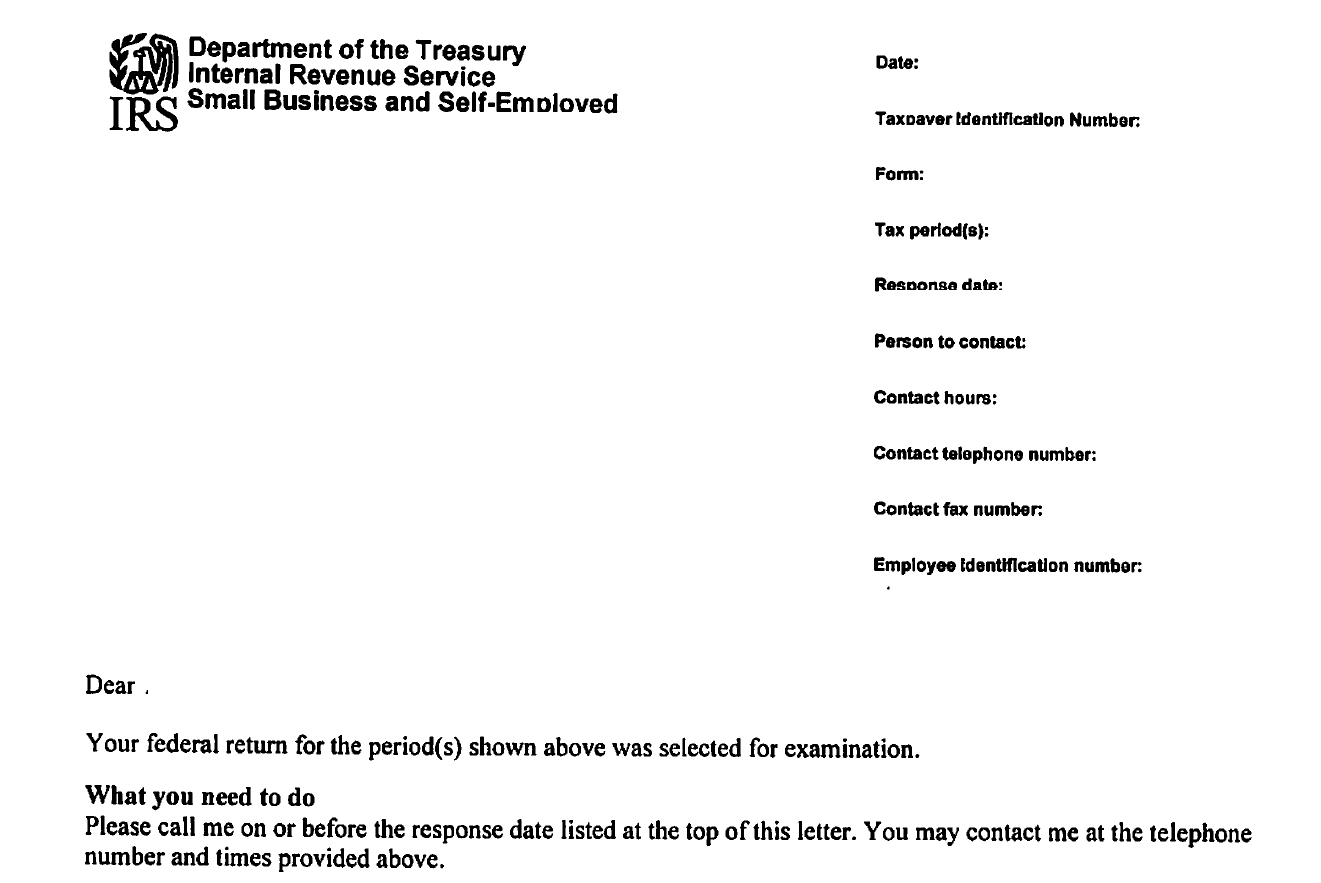

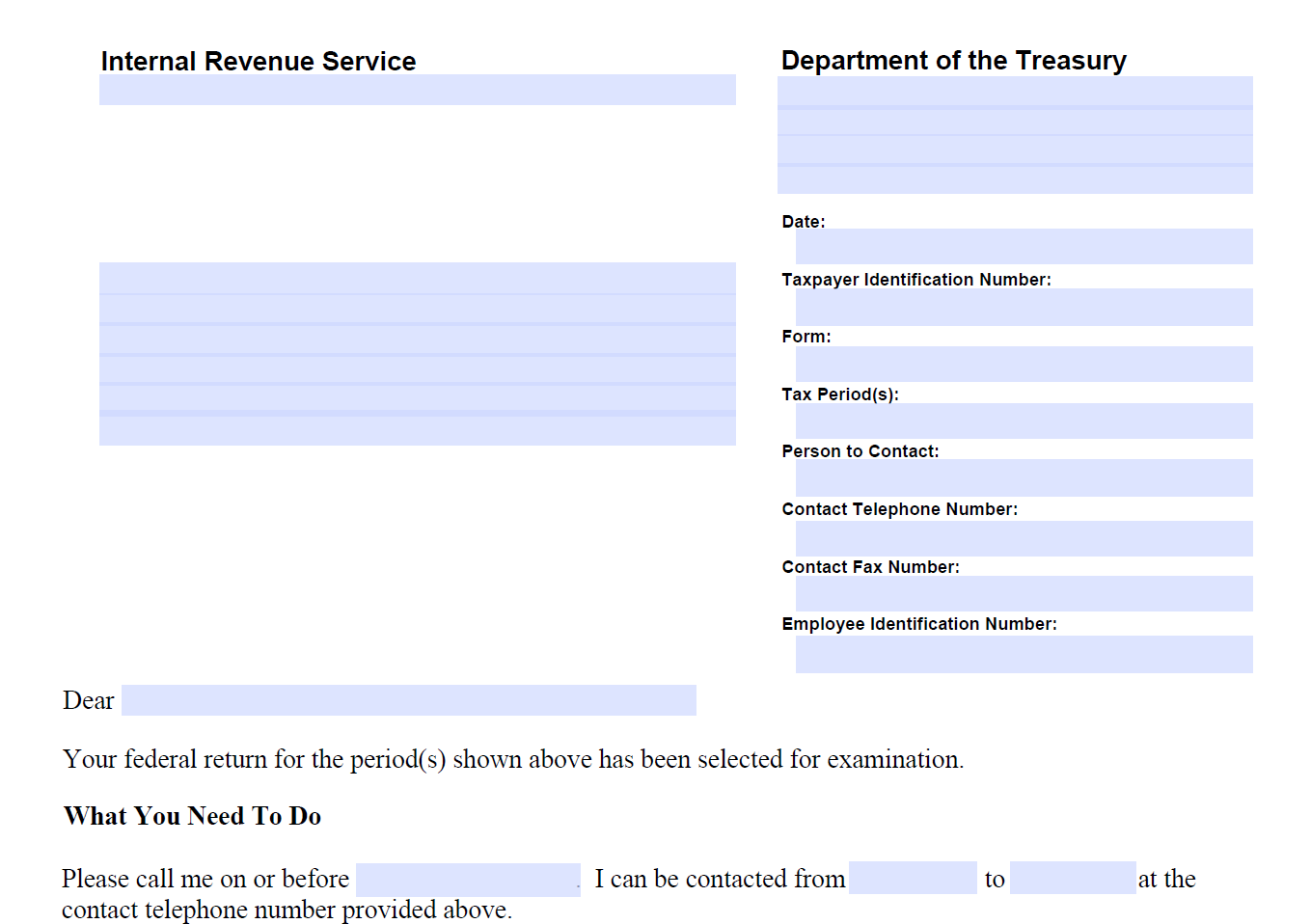

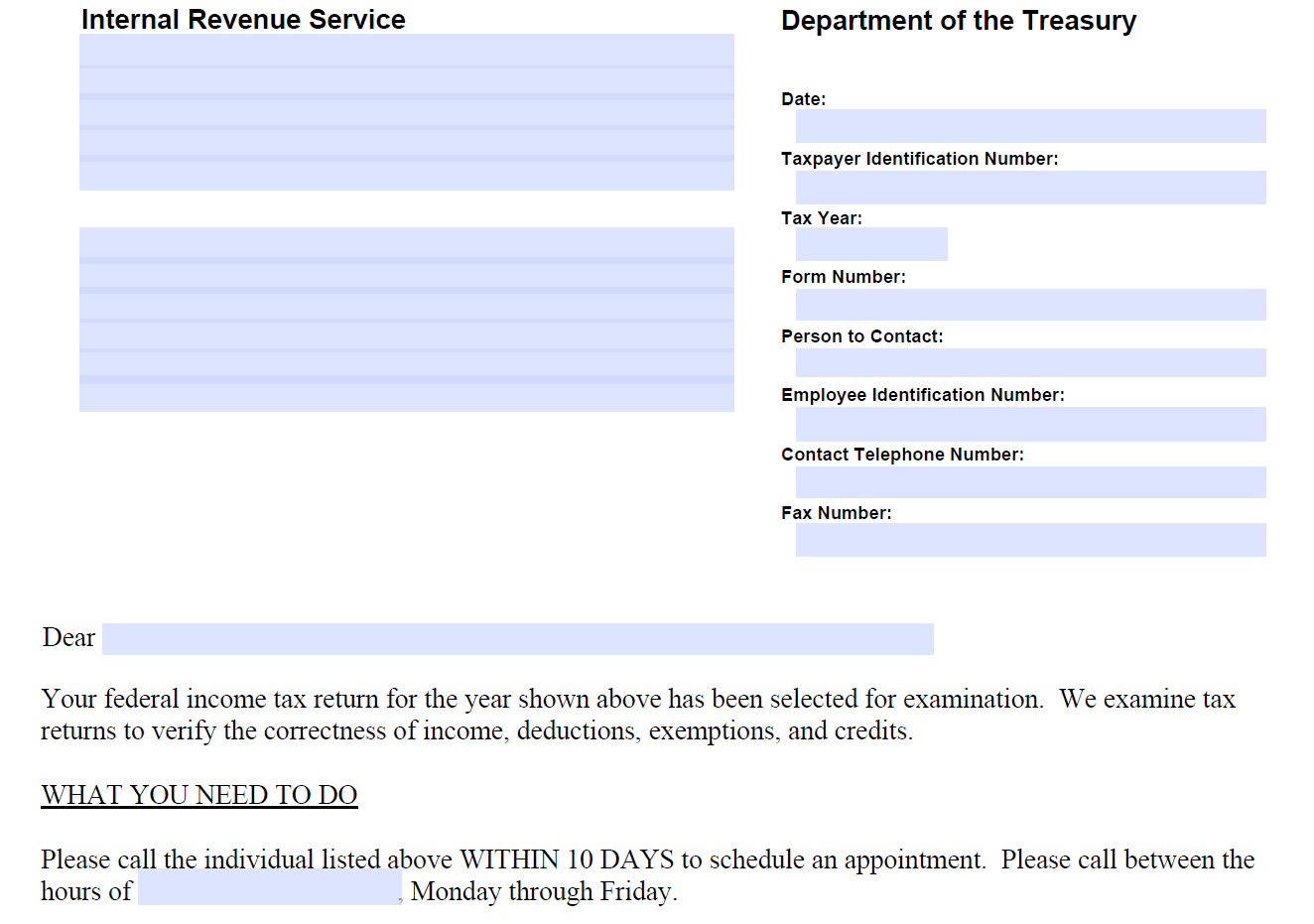

Letter 3572: SB/SE Office Exam Call-Back Appointment Letter

Office Exam: sent to request individual taxpayers who must call to schedule an initial appointment. Allows the taxpayer 14 calendar days to respond. [IRM 4.10.2.8.1.1 (11-4-2016)]

Updated: June 23, 2025