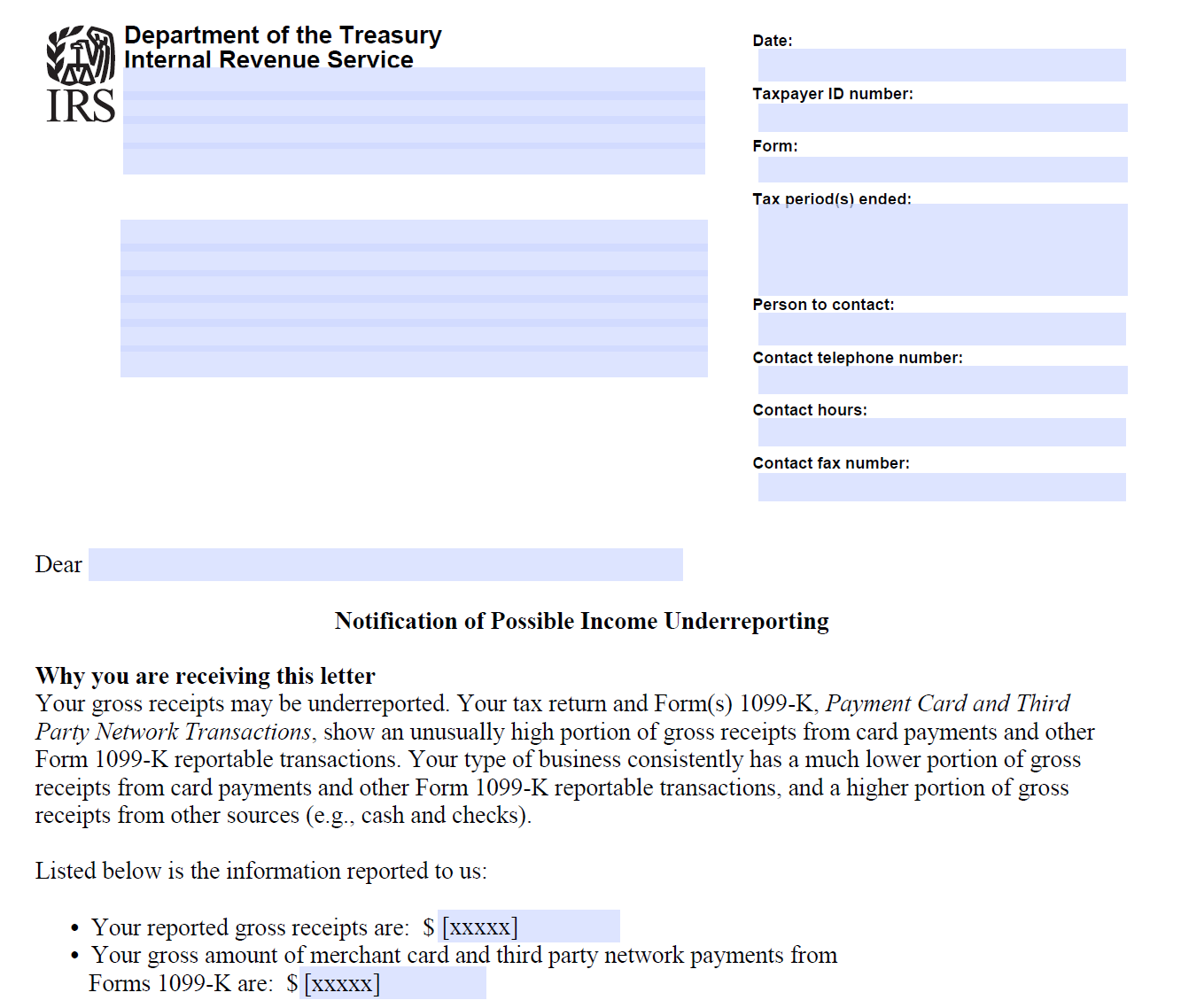

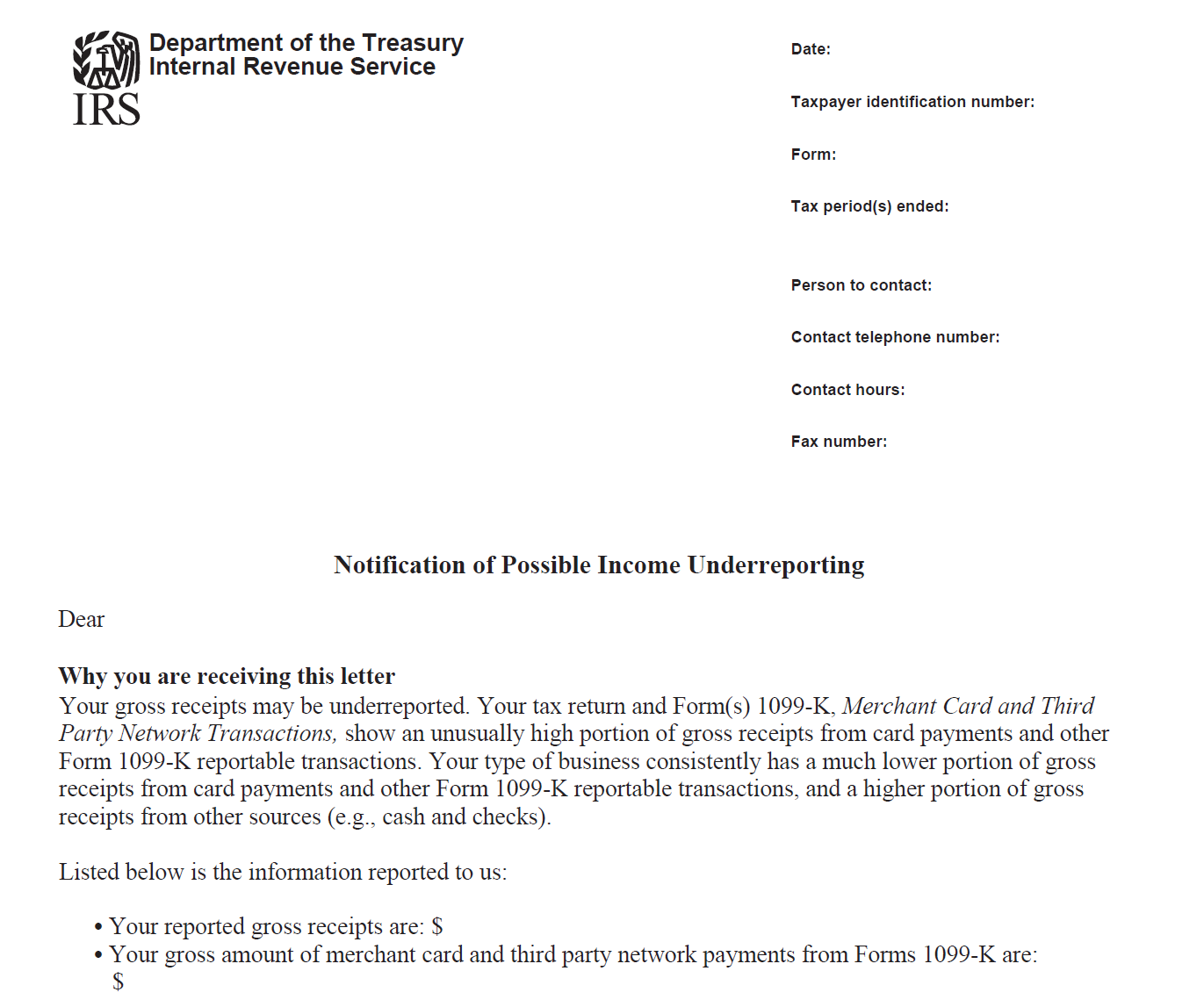

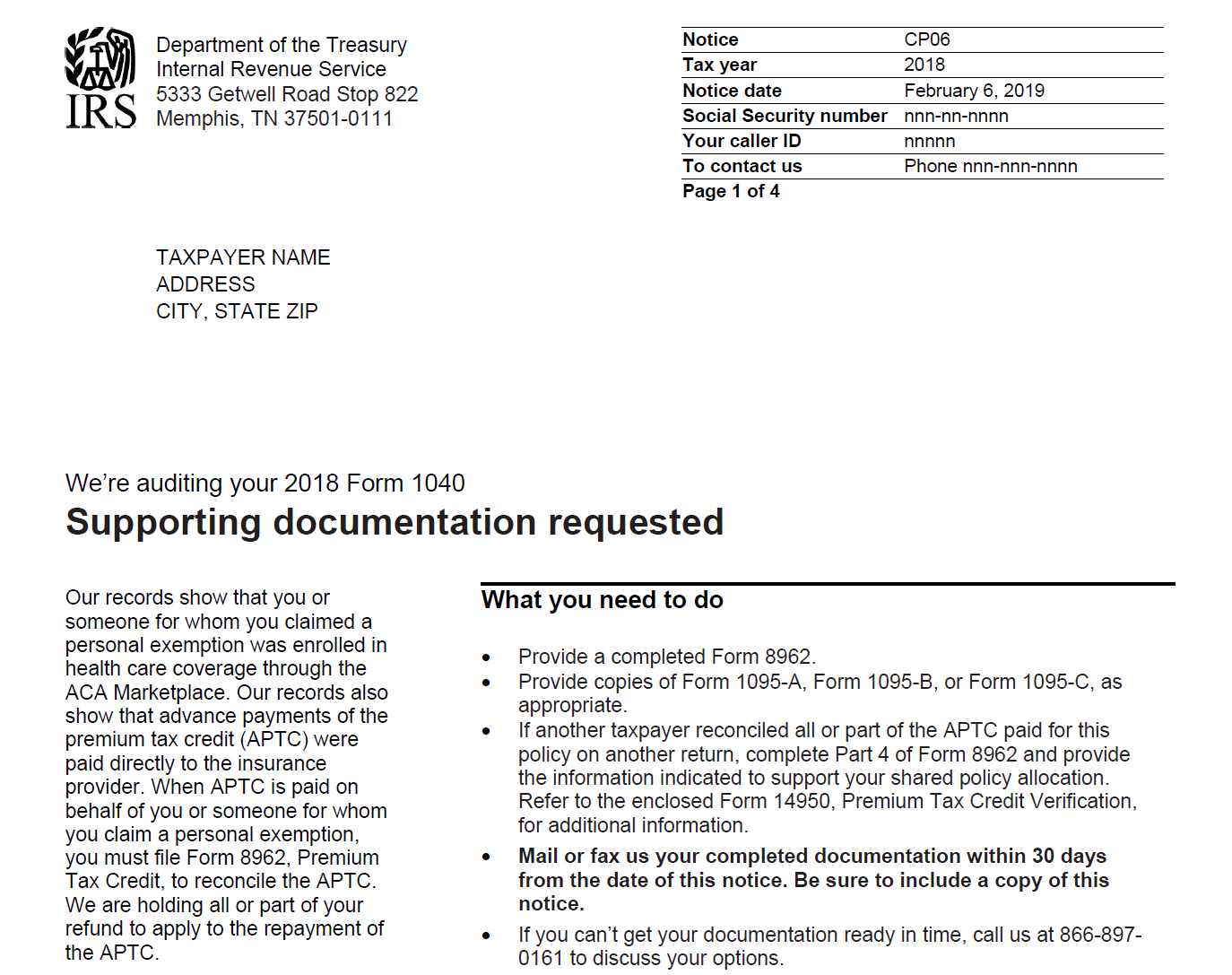

CP06: Exam Initial Contact Letter – PTC – Refund Frozen

Premium tax credit discrepancy audits in which the IRS has frozen the taxpayer’s refund until the taxpayer can prove the correctness of the PTC. [IRM 21.3.1.6.2 (10-1-2024)]

Updated: June 23, 2025